Market Statistics Report for August 1, 2024

Market Dashboard – Dashboard

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

Daily Market Snapshot

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

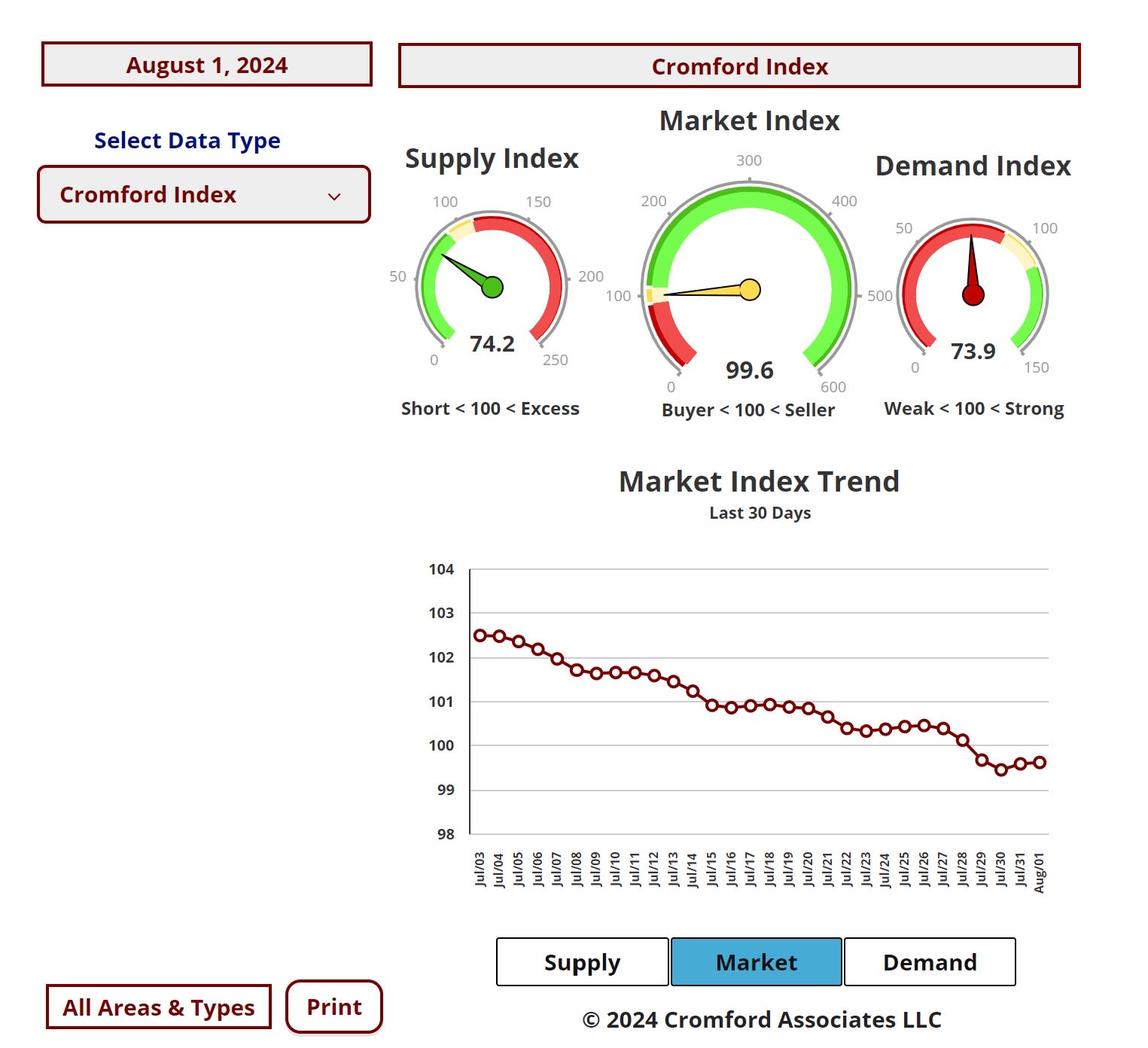

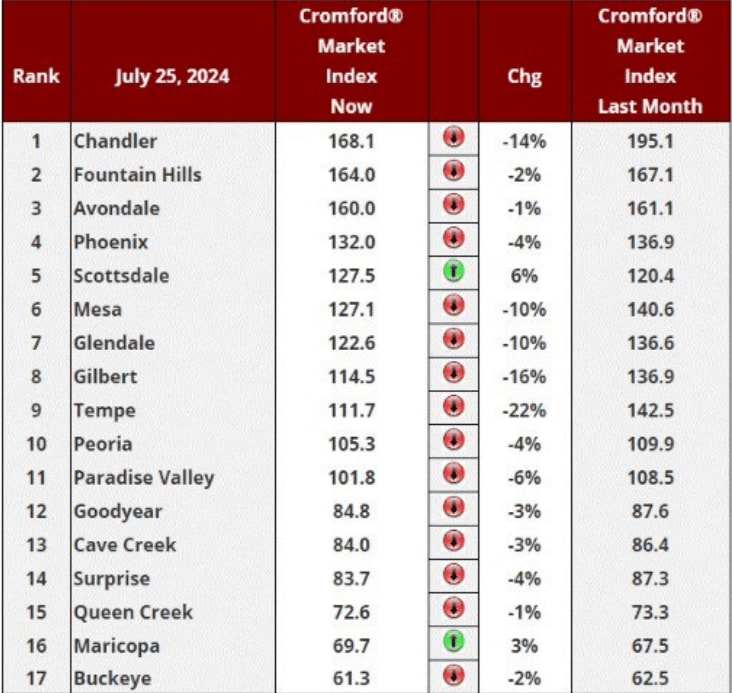

Cromford Market Index

cities.

Cromford Market Index Commentary

At first sight this looks bad. We have only 2 cities showing an increase in their Cromford® Market Index over the

past month, half as many as last week. Avondale and Queen Creek have reversed course leaving Scottsdale and

Maricopa alone. 15 have declined, so the vast majority have deteriorated for sellers. However, most of these only

fell by a small percentage. Former high-fliers Tempe, Gilbert and Chandler show the biggest falls.

After a second look, things look a lot better. The average change in CMI over the past month is -5.4%, a smaller

fall than the -6.7% we saw last week. The rate of decline has definitely changed direction, and this is a positive sign

for the market. Things are deteriorating more slowly.

9 out of 17 cities remain seller's markets over 110, though that looks unlikely to last much longer for Tempe and

Gilbert. We have 2 cities that are balanced, while the remaining 6 are buyer's markets. 3 cities still remain over

140.

One of the largest markets by dollar volume (Scottsdale) has improved by 6% over the last month. Given that we

are in the middle of the slowest season for luxury homes, this is another encouraging sign for that market.

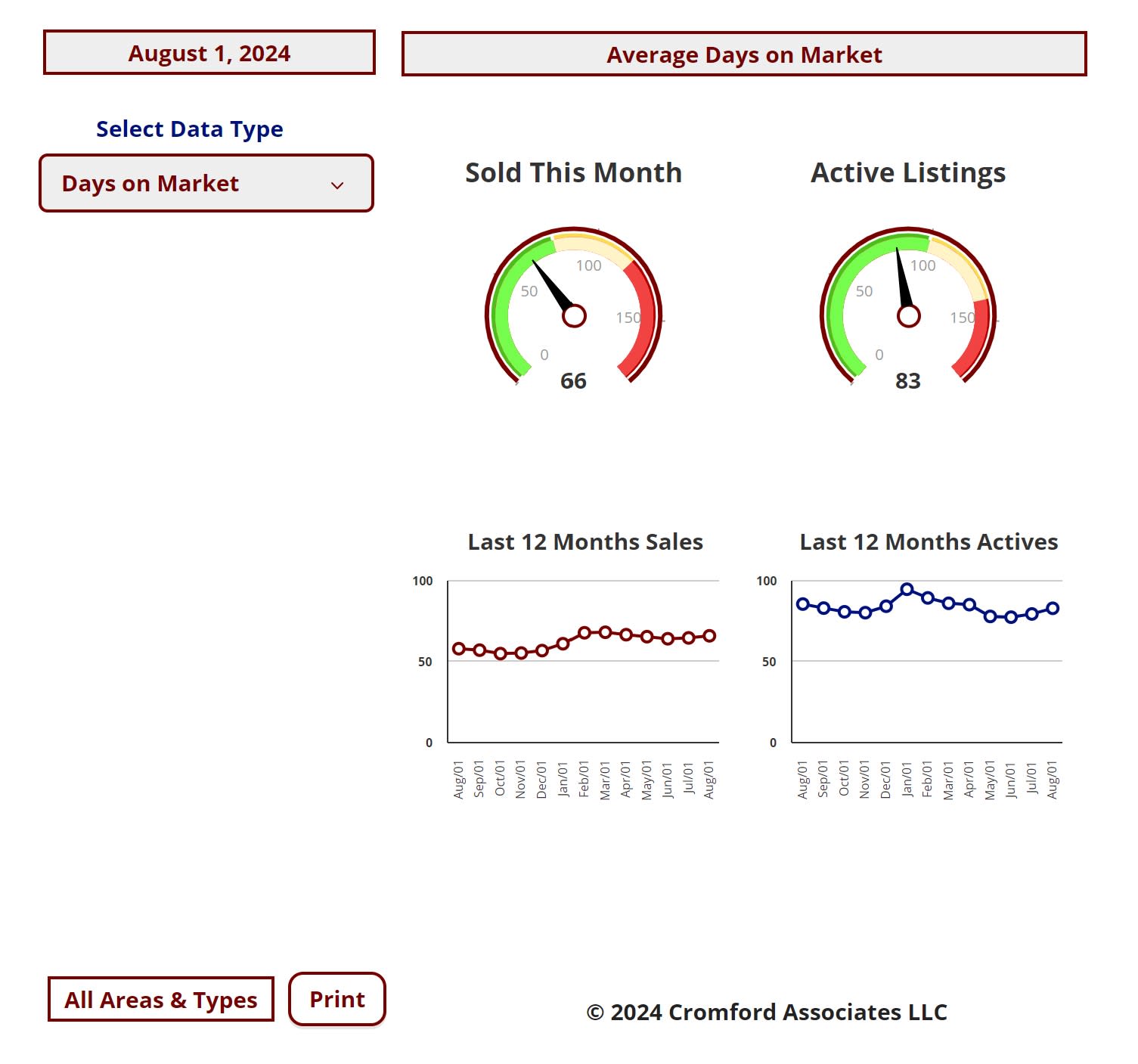

Cromford Market Index – Average Days on Market

NAR Commission Settlement Commentary

Jul 29 - With the NAR Commission Settlement imminent, there is widespread uncertainty and confusion across the

industry about how it will all play out.

The uncertainty is exemplified by the decision of the CMLS not to offer best practices advice to its members. The

Council of Multiple Listing Services (CMLS) represents 225 different MLS providers across the country and has

urged its members to have "thoughtful conversations" and "pick your own adventure". This means we are likely to

see different implementations in different geographies. The confusion is also exemplified by the NAR's FAQ

webpage on the settlement where the number of FAQs has risen to more than 100, putting it well into TLDR territory.

Recent surveys have shown that commission rates have varied little across the regions of the USA with buyer's

agents earning between 2.6% and 2.8% historically while listing agents have earned 2.8% to 3.2%. In recent

months these numbers have fallen a little to 2.4% to 2.8% and 2.8% to3.0%. There is a lack of consensus on what

these numbers might look like over the next year.

The impact of the settlement is likely to be much more significant to real estate agents than the housing market

itself, though some effects are certainly possible. Our feeling is that these would tend to reinforce existing trends

rather than change them.

We are at a low level of closing activity with only 70,473 closed listings over the past 12 months across all areas &

types. This is down from 74,060 a year ago and well below the long-term average of 85,101. We are still a long

way above the extreme low point of 48,491 that we witnessed on June 30, 2008, so there is room to fall. The

uncertain legal and procedural situation is not likely to increase volumes and we may instead see the declining

closing rate continue for some time before easing mortgage rates are able to stimulate a recovery.

New home sales may benefit from having their agent commissions clearly communicated and this could continue

to grow their percentage share of sales. Builder margins may also benefit from an increasing number of transactions

where no external agent is involved, saving them from paying any compensation to a buyer's agent or broker and

allowing them to compete harder on gross prices.

The DOJ has stated that "real estate commissions in the USA greatly exceed those in any other developed

economy" and their Antitrust Division seem determined to lower them. They want buyer's agent commissions set

between the buyer and buyer's agent and not determined at all by the seller or the selling agent. It is possible that

the NAR settlement does not go far enough for the Antitrust Division to be satisfied that this objective will be

achieved.

While it is true that real estate commissions are higher in the USA than elsewhere, the duties performed by both

buyer and listing agents are usually more extensive than in most other countries. It seems likely that when the dust

settles, buyers will end up paying lower commissions than those paid in the past on their behalf by the seller, but

buyers will also be getting a lot less advice and support during the buying process. This is not necessarily to their

advantage since a small error in buying can have major financial consequences. These can outweigh any small

difference in commission paid.

Clients tend to pay far more for legal services in the USA than in foreign countries too, but driving down the price

of legal advice will not necessarily improve or even maintain the quality of that advice.