Market Statistics Report for

December 19, 2023

Market Dashboard

This Dashboard provides a comprehensive summary of the current state of the overall residential resale market. All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County, and a small part of Yavapai County. In addition, "out of area" listings recorded on ARMLS are included, although these usually constitute a very small percentage of total sales and have very little effect on the data. All dwelling types are included. For-sale-by-owner, auctions, and other non-MLS transactions are not included. Land, commercial units, and multiple dwelling units are also excluded.

Daily Market Snapshot – City Ranking

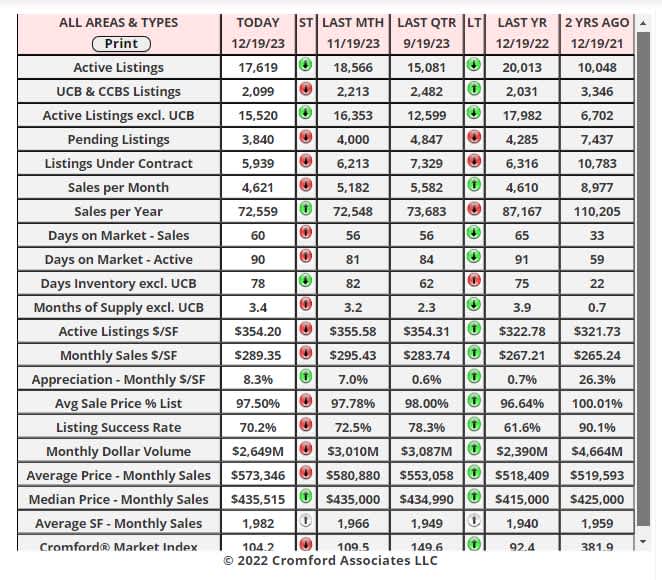

The table below provides a concise statistical summary of today's residential resale market in the Phoenix metropolitan area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

Market Index

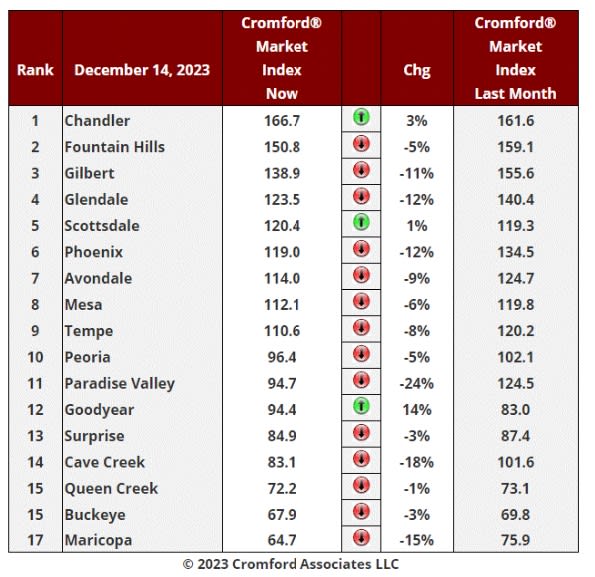

Dec 14 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest cities.

Market Index Commentary

There has been an average decline of 6.7% in the Cromford® Market Index for the 17 cities above over the last month. This is an improvement over the 9.9% decline we saw last week, but the average CMI is still significantly lower than a month ago.

We are watching to see which cities start to move in a positive direction, and this week Scottsdale has joined Goodyear and Chandler. But others, like Paradise Valley, Cave Creek, Maricopa, Glendale, and Phoenix are still showing double-digit percentage declines over the last month.

Given how much interest rates have fallen since October - and the typical 30-year fixed rate is down to 6.62% today - everyone seems to be expecting the housing market to react very positively. Indeed home-builder's stocks have been on a rampage. Our housing market numbers tell a much less exciting story. Demand has edged slightly higher in quite a few places, but given the extremely low monthly sales rates, it would take a very long time to get back to normal at the current rate of improvement. Supply normally declines sharply between Thanksgiving and New Year's Eve, but in 2023, it is barely declining at all. The market reaction to the lower rates is so far underwhelming.

9 out of 17 cities are still seller's markets, though Tempe, Mesa, and Avondale are only a tad higher than the balanced zone. We have 3 cities that are balanced and 5 that are buyer's markets. Maricopa stands out as the weakest market of the 17 with buyers having a strong negotiation advantage in that city, thanks to its plentiful supply.

We are watching to see which cities start to move in a positive direction, and this week Scottsdale has joined Goodyear and Chandler. But others, like Paradise Valley, Cave Creek, Maricopa, Glendale, and Phoenix are still showing double-digit percentage declines over the last month.

Given how much interest rates have fallen since October - and the typical 30-year fixed rate is down to 6.62% today - everyone seems to be expecting the housing market to react very positively. Indeed home-builder's stocks have been on a rampage. Our housing market numbers tell a much less exciting story. Demand has edged slightly higher in quite a few places, but given the extremely low monthly sales rates, it would take a very long time to get back to normal at the current rate of improvement. Supply normally declines sharply between Thanksgiving and New Year's Eve, but in 2023, it is barely declining at all. The market reaction to the lower rates is so far underwhelming.

9 out of 17 cities are still seller's markets, though Tempe, Mesa, and Avondale are only a tad higher than the balanced zone. We have 3 cities that are balanced and 5 that are buyer's markets. Maricopa stands out as the weakest market of the 17 with buyers having a strong negotiation advantage in that city, thanks to its plentiful supply.

Market Index Commentary – Part 2

Dec 16 - The Cromford® Market Index for all areas & types appears to have finished its decline and has settled around 104, in the balanced zone between 90 and 110. In fact, it reached a low point of 104.0 last Monday and Tuesday and has eased up to 104.2 today.

This is partly because the Demand Index has stopped declining and partly because the Supply Index has stopped rising. They are all showing little inclination to move at the moment and we probably won't get much action, or feel for direction, until we get into the second week of January.

Perhaps surprisingly, the lower interest rates have not brought a lot of new signings. The number of homes under contract is only 5,777 today, the lowest count since January 8 and well below the 6,333 we measured the same time last year. Yesterday's rate for 30-year fixed loans was 6.64%, while the 30-year FHA rate was 6.14%. These are much lower than a month ago and far below the rates in mid to late October.

It is entirely possible that buyers are waiting for January rather than committing themselves to house-hunting during December.

With the CMI above 100, we should not be seeing significant weakness in pricing, so I hope buyers are not waiting for overall price drops. Individual listings give us price cuts all the time, but these are balanced by new listings coming in at higher levels. Any price weakness is likely to be concentrated in the areas with the lowest CMI, such as Maricopa, Buckeye, Queen Creek (including San Tan Valley), Cave Creek, and Surprise. Among the smaller cities, Casa Grande, Gold Canyon, and Sun City look the weakest. In contrast, we see strength building in Apache Junction and Litchfield Park.,

This is partly because the Demand Index has stopped declining and partly because the Supply Index has stopped rising. They are all showing little inclination to move at the moment and we probably won't get much action, or feel for direction, until we get into the second week of January.

Perhaps surprisingly, the lower interest rates have not brought a lot of new signings. The number of homes under contract is only 5,777 today, the lowest count since January 8 and well below the 6,333 we measured the same time last year. Yesterday's rate for 30-year fixed loans was 6.64%, while the 30-year FHA rate was 6.14%. These are much lower than a month ago and far below the rates in mid to late October.

It is entirely possible that buyers are waiting for January rather than committing themselves to house-hunting during December.

With the CMI above 100, we should not be seeing significant weakness in pricing, so I hope buyers are not waiting for overall price drops. Individual listings give us price cuts all the time, but these are balanced by new listings coming in at higher levels. Any price weakness is likely to be concentrated in the areas with the lowest CMI, such as Maricopa, Buckeye, Queen Creek (including San Tan Valley), Cave Creek, and Surprise. Among the smaller cities, Casa Grande, Gold Canyon, and Sun City look the weakest. In contrast, we see strength building in Apache Junction and Litchfield Park.,