Market Statistics Report for

November 29, 2023

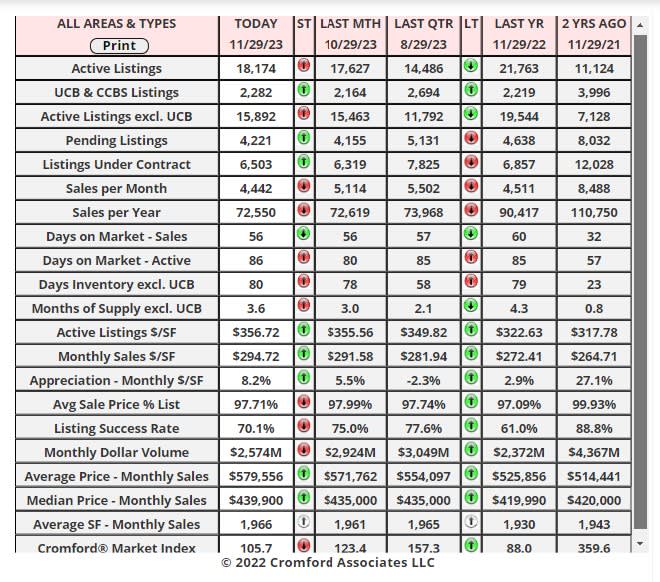

Market Dashboard

This Dashboard provides a comprehensive summary of the current state of the overall residential resale market.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County, and a small part of Yavapai County. In addition, "out of area" listings recorded on ARMLS are included, although these usually constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions, and other non-MLS transactions are not included. Land, commercial units, and multiple dwelling units are also excluded.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County, and a small part of Yavapai County. In addition, "out of area" listings recorded on ARMLS are included, although these usually constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions, and other non-MLS transactions are not included. Land, commercial units, and multiple dwelling units are also excluded.

Daily Market Snapshot – City Ranking

The table below provides a concise statistical summary of today's residential resale market in the Phoenix metropolitan area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small part of Yavapai County. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

Market Index

Nov 23 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest cities.

Market Index Commentary

There was an average decline of 15.2% in the Cromford® Market Index for the 17 cities above. This is an improvement over the 16.1% decline we saw last week, but not a very big one.

The majority of cities were worse than average, including Paradise Valley, Cave Creek, Glendale, Phoenix, Surprise, Mesa, Peoria, Maricopa, Queen Creek, Avondale, Scottsdale, and Buckeye.

Goodyear stands out as the only major city that saw its CMI improve over the last month. Also doing relatively well are Tempe, Fountain Hills, and Chandler.

10 out of 17 cities are still sellers’ markets with Peoria and Cave Creek in the balanced zone while Surprise, Buckeye, Goodyear, Queen Creek, and Maricopa are all buyers' markets. Maricopa and Queen Creek are below the 80 level and Buckeye has dropped below 70.

We are seeing a little improvement in the demand trend, but supply continues to increase in most areas, which is unusual for the third week of November.

The majority of cities were worse than average, including Paradise Valley, Cave Creek, Glendale, Phoenix, Surprise, Mesa, Peoria, Maricopa, Queen Creek, Avondale, Scottsdale, and Buckeye.

Goodyear stands out as the only major city that saw its CMI improve over the last month. Also doing relatively well are Tempe, Fountain Hills, and Chandler.

10 out of 17 cities are still sellers’ markets with Peoria and Cave Creek in the balanced zone while Surprise, Buckeye, Goodyear, Queen Creek, and Maricopa are all buyers' markets. Maricopa and Queen Creek are below the 80 level and Buckeye has dropped below 70.

We are seeing a little improvement in the demand trend, but supply continues to increase in most areas, which is unusual for the third week of November.

Active Listings

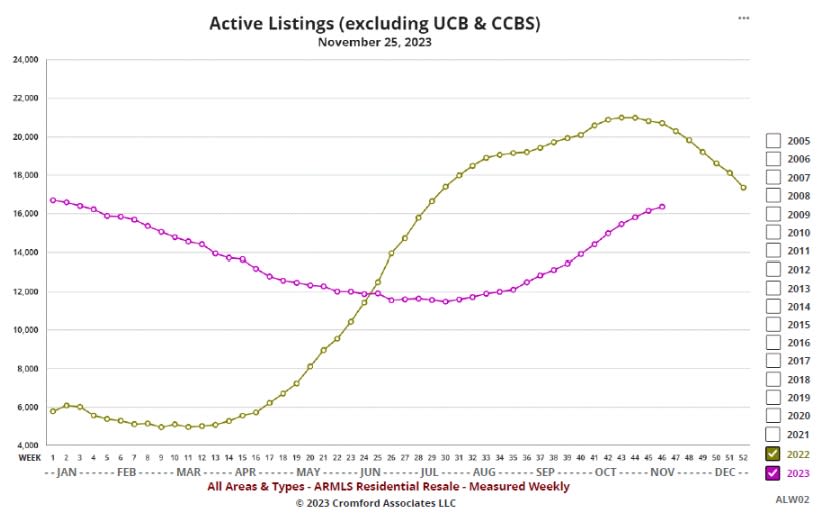

Nov 25 - Here is the weekly chart of active listing counts for all areas & types for 2022 and 2023:

We can see that the count has not yet stopped rising although the rate of increase is slowing down. Last year we saw the count decline from early November. We appear destined to end 2023 with supply roughly the same as we started in January, around the 16,000 mark.

So far, demand is showing only a weak positive response to lower interest rates and the overall market is in a balanced situation, with sellers still having an advantage in the most sought-after locations while buyers have the edge at the fringes.

Prices continue to hold up well, probably because we don't see the widespread fear that dominated market sentiment 12 months ago. However, 12 months ago we were at a turning point where the situation started to improve, while right now we are waiting for the market to stop deteriorating.

We can see that the count has not yet stopped rising although the rate of increase is slowing down. Last year we saw the count decline from early November. We appear destined to end 2023 with supply roughly the same as we started in January, around the 16,000 mark.

So far, demand is showing only a weak positive response to lower interest rates and the overall market is in a balanced situation, with sellers still having an advantage in the most sought-after locations while buyers have the edge at the fringes.

Prices continue to hold up well, probably because we don't see the widespread fear that dominated market sentiment 12 months ago. However, 12 months ago we were at a turning point where the situation started to improve, while right now we are waiting for the market to stop deteriorating.

The latest S&P / Case-Shiller® Home Price Index® - Nov 28:

The new report covers home sales during the period July to September 2023. This means the typical home sale closed in mid-August, more than 3 months ago.

We have 15 of the 20 cities showing rising prices for last month, with a higher index for Phoenix for the seventh month in a row. However, 5 cities declined over the last month.

Comparing with the previous month's series we see the following changes:

1. Detroit +0.68%

2. New York +0.62%

3. Las Vegas +0.60%

4. Miami +0.59%

5. Phoenix +0.54%

6. Tampa +0.54%

7. Boston +0.47%

8. Charlotte +0.46%

9. Cleveland +0.33%

10. Chicago +0.27%

11. Los Angeles +0.19%

12. Washington +0.13%

13. Atlanta +0.10%

14. San Francisco +0.06%

15. San Diego +0.05%

16. Dallas -0.13%

17. Denver -0.35%

18. Portland -0.41%

19. Minneapolis -0.43%

20. Seattle -0.53%

Phoenix has risen from 6th to 5th place since last month. The national average increase month to month was +0.30%, so Phoenix remains comfortably ahead of that standard.

Comparing year over year, we see the following changes:

1. Detroit +6.7%

2. San Diego +6.5%

3. New York +6.3%

4. Chicago +6.0%

5. Boston +5.3%

6. Los Angeles +5.2%

7. Cleveland +5.1%

8. Miami +5.0%

9. Charlotte +4.7%

10. Washington +4.4%

11. Atlanta +4.3%

12. Minneapolis +2.4%

13. Tampa +1.5%

14. Denver +1.0%

15. Seattle +0.9%

16. San Francisco +0.5%

17. Dallas +0.3%

18. Portland -0.7%

19. Phoenix -1.2%

20. Las Vegas -1.9%

Phoenix lies once again in 19th place and among the weakest cities on a year-over-year basis. 17 of the 20 cities are now showing positive price movement from one year ago and once again the northern cities are looking good on the year-over-year measure, along with Southern California.

The national average is +3.9% year over year. We can see that Phoenix pricing has been much weaker than the national average between 3Q 2022 and 3Q 2023. We can also see that those predicting a nationwide housing crash over the 12 months were wrong. No surprise there.

We have 15 of the 20 cities showing rising prices for last month, with a higher index for Phoenix for the seventh month in a row. However, 5 cities declined over the last month.

Comparing with the previous month's series we see the following changes:

1. Detroit +0.68%

2. New York +0.62%

3. Las Vegas +0.60%

4. Miami +0.59%

5. Phoenix +0.54%

6. Tampa +0.54%

7. Boston +0.47%

8. Charlotte +0.46%

9. Cleveland +0.33%

10. Chicago +0.27%

11. Los Angeles +0.19%

12. Washington +0.13%

13. Atlanta +0.10%

14. San Francisco +0.06%

15. San Diego +0.05%

16. Dallas -0.13%

17. Denver -0.35%

18. Portland -0.41%

19. Minneapolis -0.43%

20. Seattle -0.53%

Phoenix has risen from 6th to 5th place since last month. The national average increase month to month was +0.30%, so Phoenix remains comfortably ahead of that standard.

Comparing year over year, we see the following changes:

1. Detroit +6.7%

2. San Diego +6.5%

3. New York +6.3%

4. Chicago +6.0%

5. Boston +5.3%

6. Los Angeles +5.2%

7. Cleveland +5.1%

8. Miami +5.0%

9. Charlotte +4.7%

10. Washington +4.4%

11. Atlanta +4.3%

12. Minneapolis +2.4%

13. Tampa +1.5%

14. Denver +1.0%

15. Seattle +0.9%

16. San Francisco +0.5%

17. Dallas +0.3%

18. Portland -0.7%

19. Phoenix -1.2%

20. Las Vegas -1.9%

Phoenix lies once again in 19th place and among the weakest cities on a year-over-year basis. 17 of the 20 cities are now showing positive price movement from one year ago and once again the northern cities are looking good on the year-over-year measure, along with Southern California.

The national average is +3.9% year over year. We can see that Phoenix pricing has been much weaker than the national average between 3Q 2022 and 3Q 2023. We can also see that those predicting a nationwide housing crash over the 12 months were wrong. No surprise there.