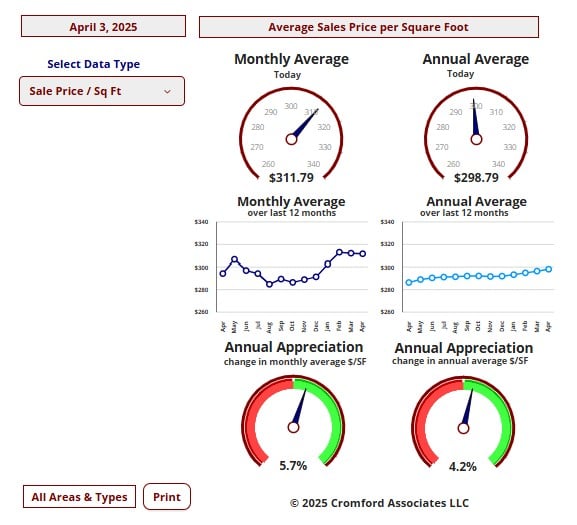

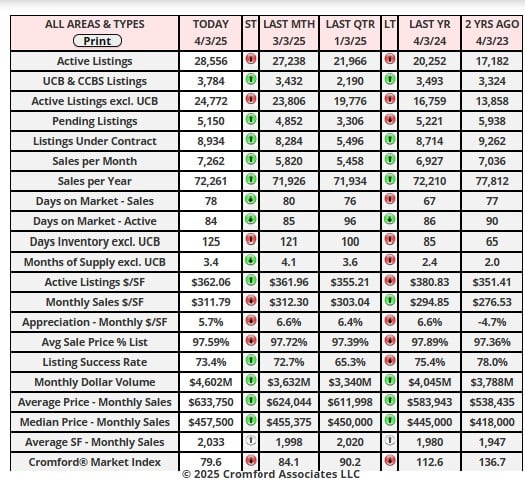

Market Statistics Report for April 3, 2025

Market Dashboard – Dashboard

This Dashboard provides a comprehensive summary of the current state of the overall residential resale market.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

commercial units, and multiple dwelling units are also excluded.

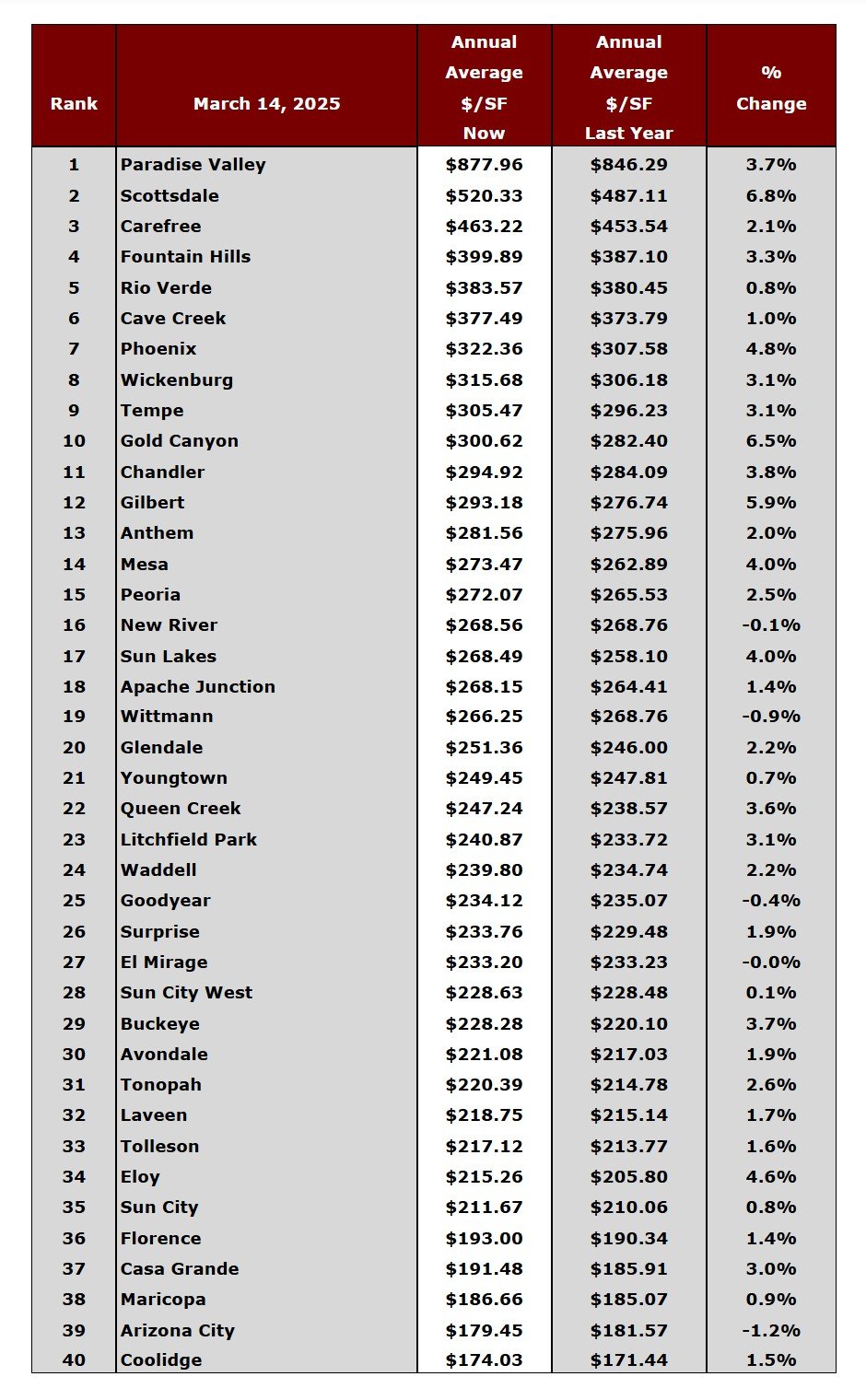

City Ranking – Snapshot

This table ranks the cities by their annual average sales price per square foot. Only single family detached homes are

included in these numbers. Information for the large and secondary cities is current as of the date shown. Data for the

11 small cities is updated on a monthly basis, and is measured on the 13th of each month.The primary function of this

table is to show the least and most affordable areas in the Phoenix metropolitan area together with longer term pricing

trends. Annual averages are based on a relatively large number of sales. Therefore they are not as subject to rapid

change as monthly averages. The downside is that they do not necessarily represent the current market very

accurately, since they include sales from up to a year ago. Pricing may have moved a great deal since then.

included in these numbers. Information for the large and secondary cities is current as of the date shown. Data for the

11 small cities is updated on a monthly basis, and is measured on the 13th of each month.The primary function of this

table is to show the least and most affordable areas in the Phoenix metropolitan area together with longer term pricing

trends. Annual averages are based on a relatively large number of sales. Therefore they are not as subject to rapid

change as monthly averages. The downside is that they do not necessarily represent the current market very

accurately, since they include sales from up to a year ago. Pricing may have moved a great deal since then.

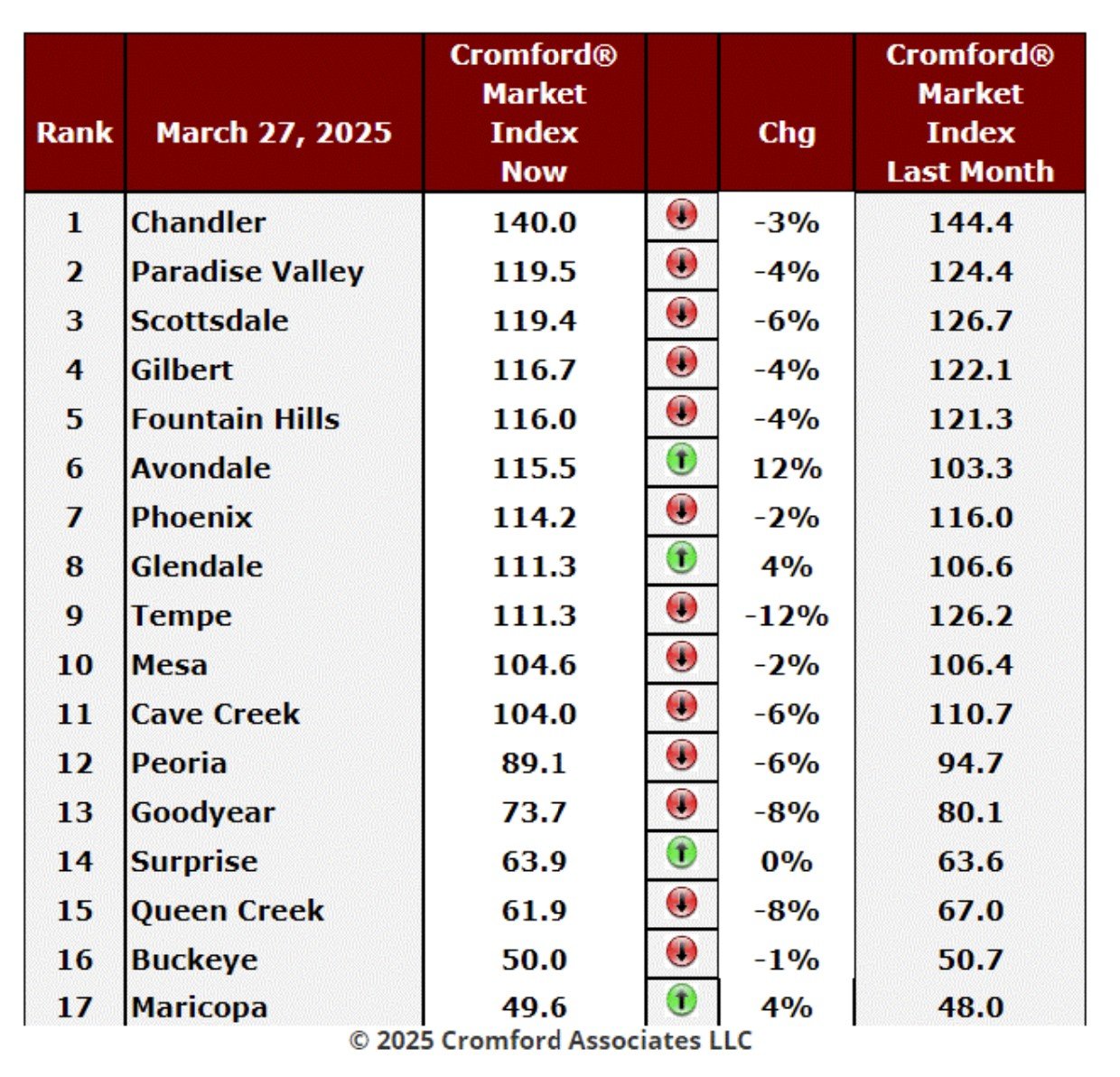

Cromford Market Index

March 27 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest

cities.

cities.

Cromford Market Index Commentary

The table is still reporting a swing in favor of buyers and the swing has started to move faster again. We

have 13 cities that have deteriorated for sellers over the last month and 4 that have improved. Avondale

is the only city with a high percentage improvement of 12%, while Glendale and Maricopa managed

4%. Surprise only gave sellers a barely detectable gain of 0.3%.

have 13 cities that have deteriorated for sellers over the last month and 4 that have improved. Avondale

is the only city with a high percentage improvement of 12%, while Glendale and Maricopa managed

4%. Surprise only gave sellers a barely detectable gain of 0.3%.

All the other cities moved in favor of buyers, with Tempe, Goodyear and Queen Creek the strongest in

that respect.

that respect.

The average change in CMI over the past month is -2.7% while last week we saw -1.9%. This continues

the trend that started last week. The difference is still only slight however.

the trend that started last week. The difference is still only slight however.

We have 9 cities that are still seller's markets, 2 that are balanced and 6 that are buyer's markets. Peoria

is the latest city to join that latter group with its CMI falling below 90%.

is the latest city to join that latter group with its CMI falling below 90%.

Today the overall Cromford® Supply Index reached 100 for the first time since May 29, 2011 - almost

14 years ago. So it is fair to say we no longer have a housing shortage. It is also fair to say we would

not have an excess supply if it were not for demand being far weaker than normal. Our overall measure

of demand (the Cromford® Demand Index) is about 19% below normal. The implication is there are

about 24% more homes for sale than we need for the present number of buyers active in the market.

Given that we are in the middle of the peak buying season, this is a serious concern.

It is a good time to be a buyer from the point of view of negotiation power, but buyers tend to lose

motivation if they start to sense prices in decline. Closed prices have been holding up very well, with

the top end of the market doing some very heavy lifting. But there is obvious weakness in the leading

indicators of price - among the active listings and listings under contract. There is now a danger that we

might enter a negative feedback loop with a deflationary cycle taking hold. Confidence that they are not

paying too high a price is a strong element of a buyer's positive mentality, and we are now in more

danger of losing that confidence than we have been in the last 15 years.

14 years ago. So it is fair to say we no longer have a housing shortage. It is also fair to say we would

not have an excess supply if it were not for demand being far weaker than normal. Our overall measure

of demand (the Cromford® Demand Index) is about 19% below normal. The implication is there are

about 24% more homes for sale than we need for the present number of buyers active in the market.

Given that we are in the middle of the peak buying season, this is a serious concern.

It is a good time to be a buyer from the point of view of negotiation power, but buyers tend to lose

motivation if they start to sense prices in decline. Closed prices have been holding up very well, with

the top end of the market doing some very heavy lifting. But there is obvious weakness in the leading

indicators of price - among the active listings and listings under contract. There is now a danger that we

might enter a negative feedback loop with a deflationary cycle taking hold. Confidence that they are not

paying too high a price is a strong element of a buyer's positive mentality, and we are now in more

danger of losing that confidence than we have been in the last 15 years.

Significantly lower mortgage interest rates could help a lot, but desire for these still seem a little

unrealistic given the persistence of inflation above the Federal Reserve target. We can still hope for a

pleasant surprise, but we cannot depend on it.

unrealistic given the persistence of inflation above the Federal Reserve target. We can still hope for a

pleasant surprise, but we cannot depend on it.

City Ranking