Market Statistics Report for December 12, 2024

Market Dashboard – Dashboard

This Dashboard provides a comprehensive summary of the current state of the overall residential resale market.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

commercial units, and multiple dwelling units are also excluded.

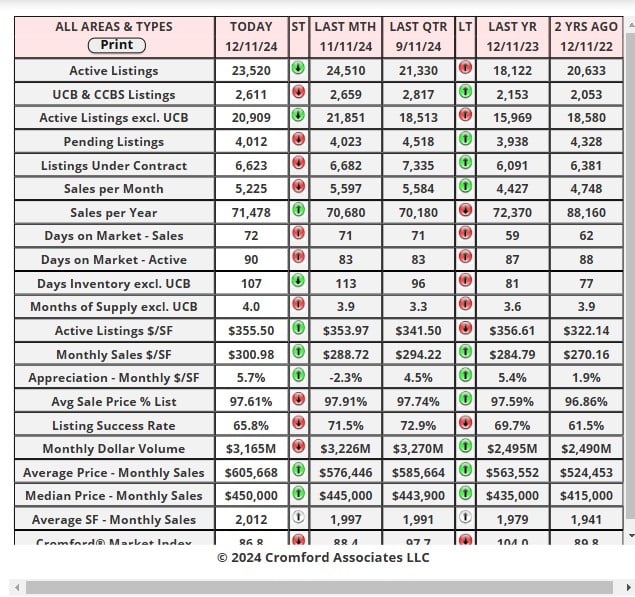

Daily Market Snapshot

The table below provides a concise statistical summary of today's residential resale market in the Phoenix metropolitan

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

Cromford Market Index

Dec 5 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest

cities.

cities.

Cromford Market Index Commentary

Just like last week, we have 6 large cities showing an increase in their Cromford® Market Index over

the past month and 11 showing a decrease. However, the average change in CMI over the past month

is -2.1% while last week we saw -3.5%. Although the market has deteriorated for sellers over the month,

it is starting to benefit from falling supply. This is nothing to get excited about since it happens every

December. But the fact that it happened again in 2024 is reassuring us that the world has not completely

changed.

the past month and 11 showing a decrease. However, the average change in CMI over the past month

is -2.1% while last week we saw -3.5%. Although the market has deteriorated for sellers over the month,

it is starting to benefit from falling supply. This is nothing to get excited about since it happens every

December. But the fact that it happened again in 2024 is reassuring us that the world has not completely

changed.

Fountain Hills is once again the worst performer, losing 16% over the most recent month, while Paradise

Valley is the best performer, rising 14%. Other cities improved by 3% or less, except for Tempe which

is up 7% and has moved from a balanced market to a seller's market.

Buckeye, Surprise, Maricopa, Peoria, Cave Creek and Mesa deteriorated by 6% or more.

Valley is the best performer, rising 14%. Other cities improved by 3% or less, except for Tempe which

is up 7% and has moved from a balanced market to a seller's market.

Buckeye, Surprise, Maricopa, Peoria, Cave Creek and Mesa deteriorated by 6% or more.

We have 6 cities that are seller's markets, though 4 of these are very weak seller's markets at less than

120. 6 cities are balanced and 5 are buyer's markets.

120. 6 cities are balanced and 5 are buyer's markets.

Maricopa and Buckeye remain very weak with excess inventory relative to current levels of demand.

It is clear that the market is weaker in outlying areas and at the lower end of the market. The central

areas and high-end are experiencing conditions that are more favorable, though not excessively so.

It is clear that the market is weaker in outlying areas and at the lower end of the market. The central

areas and high-end are experiencing conditions that are more favorable, though not excessively so.

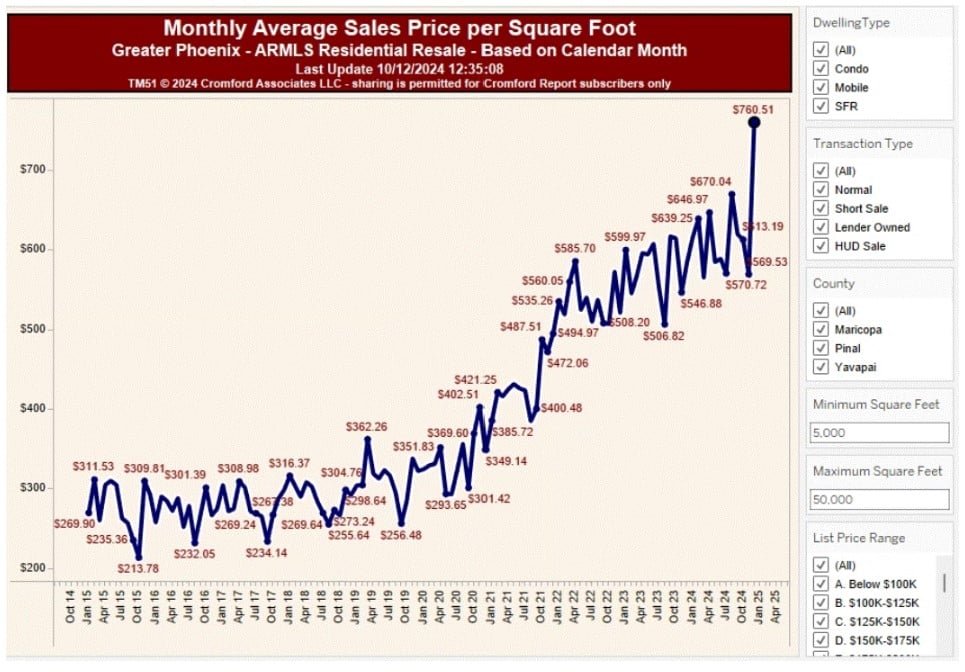

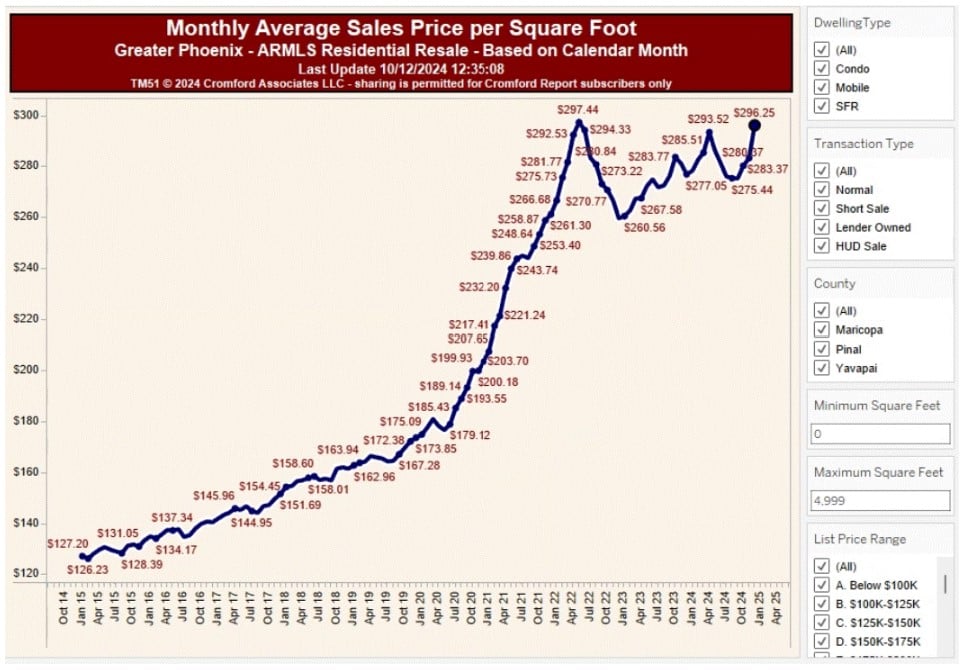

Monthly Average Sales Price per Square Foot

Dec 10 - You may have noticed a surprising increase in the average $/SF for closed listings in

December. This has been largely driven by the luxury market where we have seen a strong number of

closings at an unusually high price per square foot in the last 9 days. Average pricing for homes with

living space of 5,000 sq. ft. or more stands at $760 per sq. ft. for December month to date. This is an

amazing $90 higher than any prior month.

December. This has been largely driven by the luxury market where we have seen a strong number of

closings at an unusually high price per square foot in the last 9 days. Average pricing for homes with

living space of 5,000 sq. ft. or more stands at $760 per sq. ft. for December month to date. This is an

amazing $90 higher than any prior month.

Of course, the sample size is small at these levels. There have been only 28 closings so far this month

for homes over 5,000 sq. ft. However, this is a higher-than usual number for the first week of December

and there are several spectacular properties at eye-watering prices. Examples include:

for homes over 5,000 sq. ft. However, this is a higher-than usual number for the first week of December

and there are several spectacular properties at eye-watering prices. Examples include:

• MLS 6700989 - Paradise Valley 7,607 sq. ft. sold for $9,500,000 on Dec 2. It was built new in 2020 and

cost $4,700,000 in February that year. It has changed hands twice since than and double in price in

under 5 years. (Katrina Barrett as the selling agent!)

cost $4,700,000 in February that year. It has changed hands twice since than and double in price in

under 5 years. (Katrina Barrett as the selling agent!)

• MLS 6667094 - Paradise Valley 7,493 sq. ft. sold for $9,450,000 (brand new). (Katrina Barrett as the

selling agent!)

selling agent!)

Things are far more stable below 5,000 sq. ft.

A respectable $296 per sq. ft. but not quite beating the previous peak of $297 in May 2022. Among

these smaller homes there is still one with a $/SF over $1,200,

these smaller homes there is still one with a $/SF over $1,200,

These charts tell an interesting story.

Between 2014 and 2020 homes of 5,000 sq. ft. or more hardly saw any appreciation, but this all changed

with the COVID epidemic, and they have not stopped rising since.

with the COVID epidemic, and they have not stopped rising since.

Between 2014 and 2020 homes below 5,000 sq. ft. appreciated well but really took off during the COVID

epidemic. However, since mid-2022 prices have only moved sideways.

epidemic. However, since mid-2022 prices have only moved sideways.

The percentage gap between the general market and the high-end pricing has never been higher than

it is today. Luxury buyers are paying the highest premium we have recorded.

it is today. Luxury buyers are paying the highest premium we have recorded.

Dec 6 - The affidavits of value have been counted and analyzed for Maricopa County's November filings

and here is what we found:

and here is what we found:

• There were 5,393 closed transactions, up 10.4% from 4,887 in November 2023 but down 12.3% from

October.

October.

• There were 1,295 closed new homes, up 6.1% from 1,220 in November 2023 but down 13.8% from

October.

October.

• There were 4,098 closed re-sale transactions, up 11.8% from 3,667 in November 2023 but down 11.8%

from October.

from October.

• The overall median sales price in October was $474,790, up 2.1% from November 2023 but down

0.04% from October.

0.04% from October.

• The new home median sales price was $504,490, down 0.1% from November 2023 and down 4.0%

from October.

from October.

• The re-sale median sales price was $458,500, up 2.6% from November 2023 and up 0.8% from

October.

October.

There were 19 working days in November 2024 versus 20 in November 2023, so the 10.4% increase

in closings was despite a 5% headwind. Re-sales increased more than new homes, though both new

and re-sale transaction rates were better than last year.

in closings was despite a 5% headwind. Re-sales increased more than new homes, though both new

and re-sale transaction rates were better than last year.

New home market share fell to 24.4% in October 2024, and this is down from 26.7% a year ago.

Overall median prices were slightly lower than last month but higher than a year ago. Re-sale pricing

moved higher while new home pricing declined.

Overall median prices were slightly lower than last month but higher than a year ago. Re-sale pricing

moved higher while new home pricing declined.

New homes took a market share of 24.0%, down from 24.4% last month and 25.0% a year ago.

These numbers are for single family and townhouse / condo homes.