Market Statistics Report for January 12, 2025

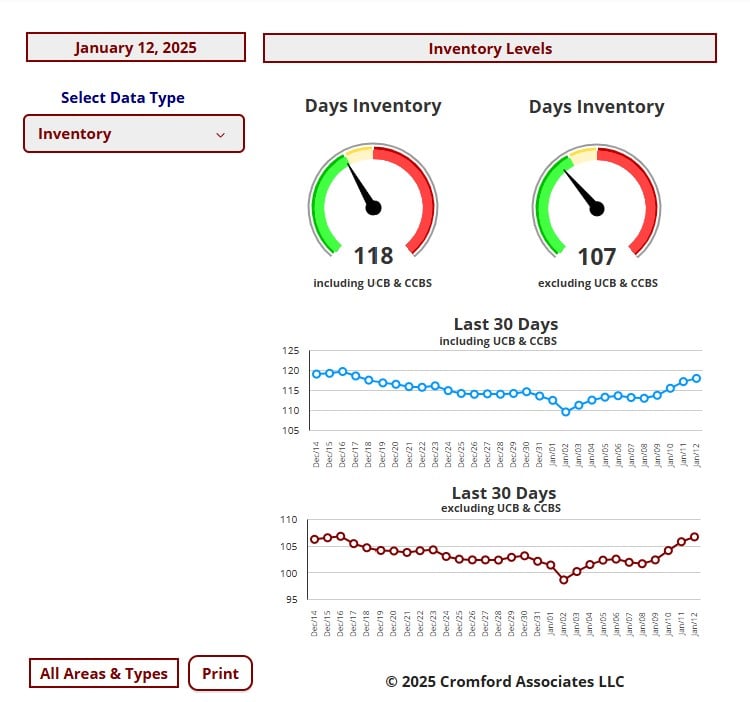

Market Dashboard – Inventory

This Dashboard provides a comprehensive summary of the current state of the overall residential resale market.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

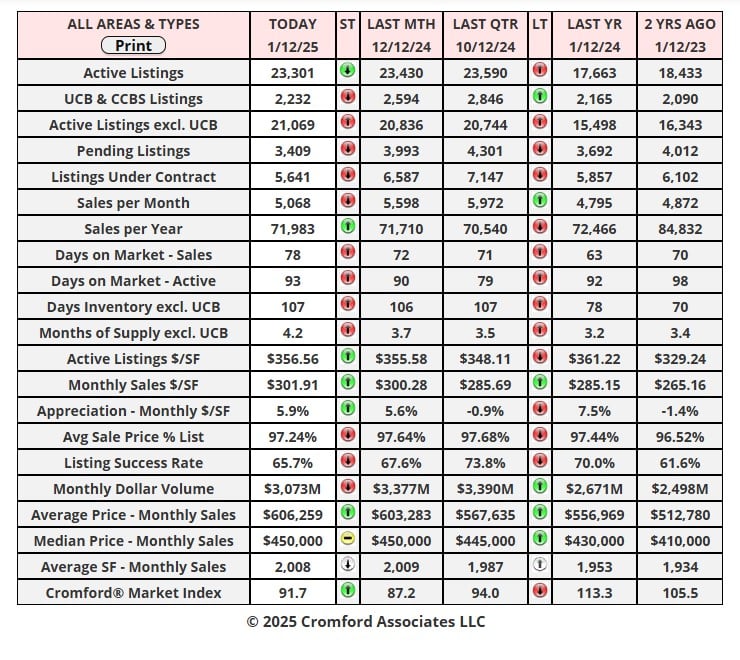

Daily Market Snapshot

The table below provides a concise statistical summary of today's residential resale market in the Phoenix metropolitan

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

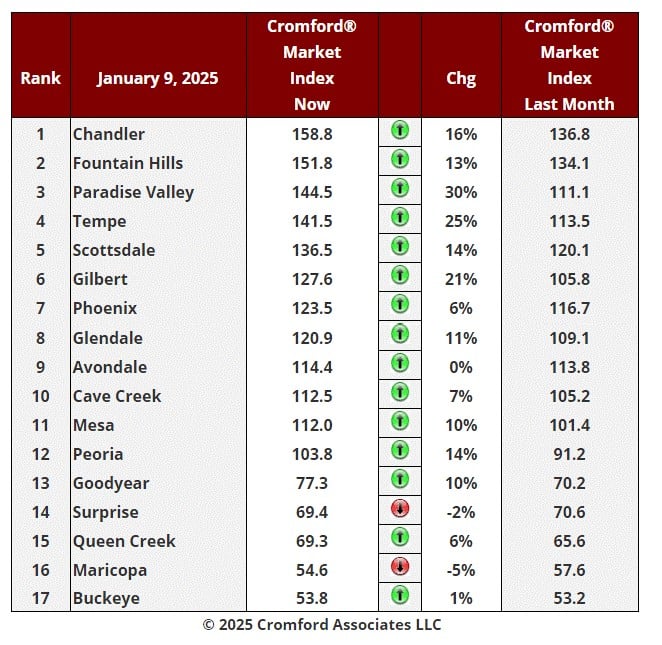

Cromford Market Index

Jan 9 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest

cities.

Cromford Market Index Commentary

Like last week, we see the market has improved significantly for sellers over the last month. We have

15 large cities showing an increase in their Cromford® Market Index over the past month and only 2

showing a decrease. These are the same cities as last week.

The average change in CMI over the past month is +10.4% while last week we saw +8.8%.

Tempe, Paradise Valley, Fountain Hills, Chandler, Scottsdale, Mesa, Glendale, Goodyear, Peoria and

Gilbert are all giving us double figure percentage improvements. The only cities that have still not

managed an improvement from one month ago are Maricopa and Surprise.

Unlike last week, we now have 11 cities that are seller's markets, only 1 that is balanced but still 5 that

are buyer's markets. Those 5 still have a long way to go to get back to balance.

Market Trends – 1st Week of January

Jan 10 - Time to take a look at the trends of the first full week of 2025.

• Active listings with no contract - these have increased 4.1% over the past week from 19,776 to 20,583

• Listings under contract - these have increased 4.4% over the past week from 5,496 to 5,737

• The contract ratio has moved very slightly higher from 27.79 to 27.87

We are trying to get a handle on the direction of the market, but to be honest there is not much to talk

about here. It's nice that listings under contract expanded by a higher percentage than active listings,

but the difference was so small it only added 0.29% to the contract ratio. This is not signaling a big

swing in favor of sellers, just more of the same as implied by a Cromford® Market Index in the low 90s.

If we compare it to the same week last year then

• Active listings have grown a bit faster - last year they increased only 3.3%

• Listings under contract have grown much slower - last year they increased 8.4%, almost twice the

percentage

• Last year the contract ratio grew from 35.98 to 37.76, adding 4.9% during the first week

• Listings under contract have grown much slower - last year they increased 8.4%, almost twice the

percentage

• Last year the contract ratio grew from 35.98 to 37.76, adding 4.9% during the first week

With mortgage rates still rising, there is little fuel for the optimists to run on here. On the other hand

there is not much to please the pessimists either.

In fact there is not much message in these numbers. Perhaps things will get more exciting during the

second week?

Market Summary for the Beginning of 2025

there is not much to please the pessimists either.

In fact there is not much message in these numbers. Perhaps things will get more exciting during the

second week?

Market Summary for the Beginning of 2025

Here are the basics - the ARMLS numbers for January 1, 2025 compared with January 1,

2024 for all areas & types:

• Active Listings (excluding UCB & CCBS): 20,007 versus 14,593 last year - up 37% - but down

7.3% from 21,593 last month

• Active Listings (including UCB & CCBS): 22,196 versus 16,457 last year - up 35% - but down 8.2%

compared with 24,178 last month

• Pending Listings: 3,307 versus 3,263 last year - up 1.3% - but down 13.2% from 3,808 last month

• Under Contract Listings (including Pending, CCBS & UCB): 5,496 versus 5,127 last year - up 7.2%

- but down 14% from 6,393 last month

• Monthly Sales: 5,581 versus 4,923 last year - up 13.4% - and up 8.4% from 5,147 last month

• Monthly Average Sales Price per Sq. Ft.: $303.62 versus $284.40 last year - up 6.8% - and up

4.7% from $290.02 last month

• Monthly Median Sales Price: $450,000 versus $429,900 last year - up 4.7% - but unchanged from

$450,000 last month

7.3% from 21,593 last month

• Active Listings (including UCB & CCBS): 22,196 versus 16,457 last year - up 35% - but down 8.2%

compared with 24,178 last month

• Pending Listings: 3,307 versus 3,263 last year - up 1.3% - but down 13.2% from 3,808 last month

• Under Contract Listings (including Pending, CCBS & UCB): 5,496 versus 5,127 last year - up 7.2%

- but down 14% from 6,393 last month

• Monthly Sales: 5,581 versus 4,923 last year - up 13.4% - and up 8.4% from 5,147 last month

• Monthly Average Sales Price per Sq. Ft.: $303.62 versus $284.40 last year - up 6.8% - and up

4.7% from $290.02 last month

• Monthly Median Sales Price: $450,000 versus $429,900 last year - up 4.7% - but unchanged from

$450,000 last month

There is quite a lot of positive news in these numbers. Obviously, supply is down from the

November peak, but we would expect that as part of the usual seasonal pattern. What we don't

know is how fast supply will grow again in January and we will be closely watching that over the

next several weeks. The decline was late starting in November, but it really accelerated in

November peak, but we would expect that as part of the usual seasonal pattern. What we don't

know is how fast supply will grow again in January and we will be closely watching that over the

next several weeks. The decline was late starting in November, but it really accelerated in

December and ended in a big bang with a large number of listings expiring at the end of December.

For sellers it is much better to have 7.3% fewer active listings to compete with. But if those expiring

listings come straight back in January, the good news will have been an illusion.

For sellers it is much better to have 7.3% fewer active listings to compete with. But if those expiring

listings come straight back in January, the good news will have been an illusion.

Closed sales counts are improving nicely. December's count was up more than 13% from a year

ago, although we must admit this was an easy target to beat. It is encouraging that the annual

sales count has risen to almost 72,000. much healthier than the 69,627 we saw at the end of

September. However, it is still well below the long-term average of 85,000 per year.

Under contract counts remain subdued but at least we managed a 7% increase from the beginning

of 2024.

ago, although we must admit this was an easy target to beat. It is encouraging that the annual

sales count has risen to almost 72,000. much healthier than the 69,627 we saw at the end of

September. However, it is still well below the long-term average of 85,000 per year.

Under contract counts remain subdued but at least we managed a 7% increase from the beginning

of 2024.

A combination of reduced supply and a slight recovery in demand means the Cromford® Market

Index has returned to the balanced zone between 90 and 110. We are no longer in a buyer's market

across all areas, though several outlying locations remain very favorable to buyers.

Index has returned to the balanced zone between 90 and 110. We are no longer in a buyer's market

across all areas, though several outlying locations remain very favorable to buyers.

Overall, demand is slowly starting to rebuild, despite mortgage rates remaining stubbornly high.

Our concern is that we do not know how much new supply will arrive during the next 3 months. If

we get a light load then the market will continue to move towards balance. If we get a large number

of new listings then we could slip back into a buyer's market. The next 4 weeks are likely to be

critical.

Pricing was unusually strong in December, particularly when we look at the $/SF numbers. This

measure is distorted by the relatively hot market in upscale luxury homes. These are selling in

healthy numbers and for higher prices. A frothy stock market, combined with elevated

cryptocurrency values means that those with significant capital investments are feeling much better

off. The very wealthy have done extremely well over the past couple of years and as usual this has

increased demand in the extremely high-end markets, especially the Northeast Valley.

we get a light load then the market will continue to move towards balance. If we get a large number

of new listings then we could slip back into a buyer's market. The next 4 weeks are likely to be

critical.

Pricing was unusually strong in December, particularly when we look at the $/SF numbers. This

measure is distorted by the relatively hot market in upscale luxury homes. These are selling in

healthy numbers and for higher prices. A frothy stock market, combined with elevated

cryptocurrency values means that those with significant capital investments are feeling much better

off. The very wealthy have done extremely well over the past couple of years and as usual this has

increased demand in the extremely high-end markets, especially the Northeast Valley.

Most home builders' stocks tell quite an interesting story in 2024 having gained hugely in value by

the end of September only to give most or all of those gains back by the end of December once it

became clear that mortgage rates were not coming down in a hurry. The inventory of completed

but unsold new homes has recently been increasing for the USA as a whole and the new home

supply is more plentiful than it was this time last year. This may lead to more flexibility from home

builders in sales negotiations during the first half of 2025, especially concerning homes that are

ready to move in.

the end of September only to give most or all of those gains back by the end of December once it

became clear that mortgage rates were not coming down in a hurry. The inventory of completed

but unsold new homes has recently been increasing for the USA as a whole and the new home

supply is more plentiful than it was this time last year. This may lead to more flexibility from home

builders in sales negotiations during the first half of 2025, especially concerning homes that are

ready to move in.

With 30-year fixed mortgage rates over 7%, we do not anticipate strong growth in demand, but the

reversal of the earlier declining demand trend is a good sign that we have seen the worst.

reversal of the earlier declining demand trend is a good sign that we have seen the worst.

Everything now depends on how much additional supply will arrive over the next few months.