Market Statistics Report for November 22, 2024

Market Dashboard – Dashboard

This Dashboard provides a comprehensive summary of the current state of the overall residential resale market.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

commercial units, and multiple dwelling units are also excluded.

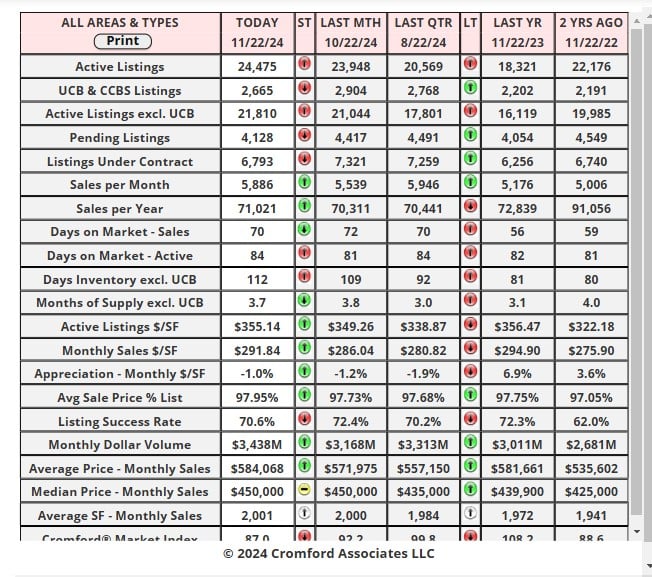

Daily Market Snapshot

The table below provides a concise statistical summary of today's residential resale market in the Phoenix metropolitan

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

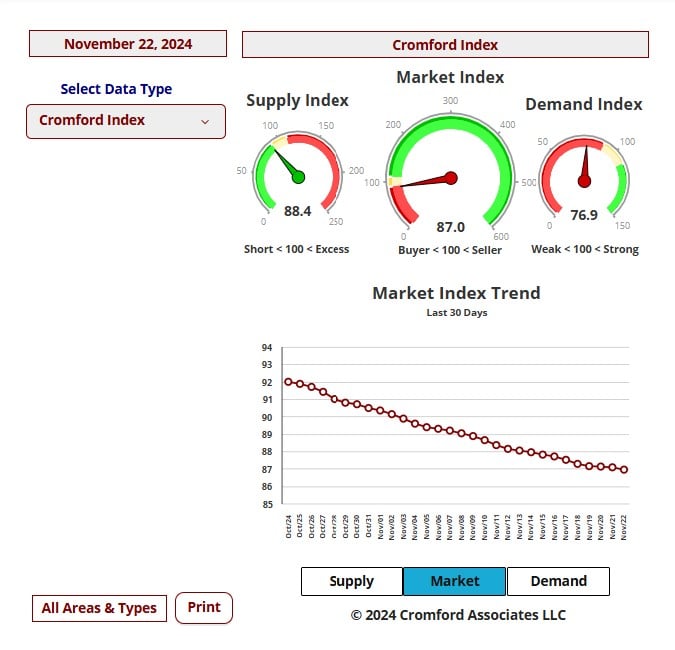

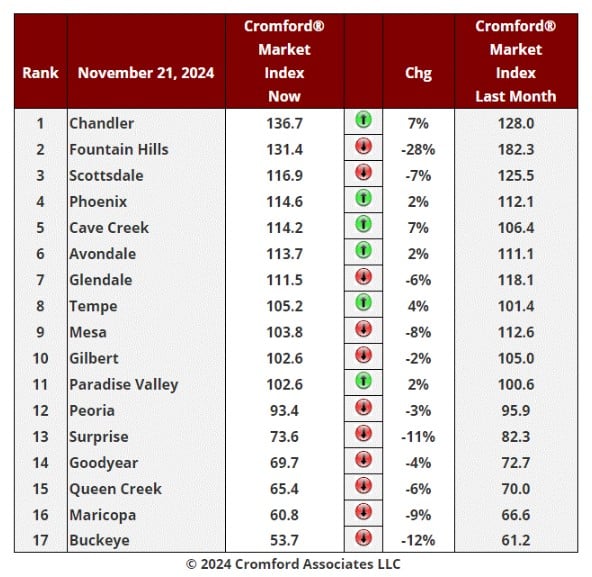

Cromford Market Index

Nov 21 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest

cities.

cities.

Cromford Market Index Commentary

Like last week, we have 6 large cities showing an increase in their Cromford® Market Index over the

past month. The average change in CMI over the past month is -4.2% while last week we saw -4.8%.

past month. The average change in CMI over the past month is -4.2% while last week we saw -4.8%.

The market is still deteriorating for sellers but less quickly than last week.

Fountain Hills is by far the worst performer, losing 28% over the most recent month and conceding first

place to Chandler, which along with Cave Creek is the best performer.

place to Chandler, which along with Cave Creek is the best performer.

Peoria has turned around and is now deteriorating while Paradise Valley has bounced back.

Buckeye, Surprise, Maricopa, Scottsdale and Mesa deteriorated by 7% or more.

Once again, we have 7 cities that are seller's markets, though 5 of these are very weak seller's markets

at less than 117. 5 cities are balanced and 5 are buyer's markets.

at less than 117. 5 cities are balanced and 5 are buyer's markets.

Nov 19 - The Cromford® Market Index for all areas and types has descended to 87.1 today. While this

is not far below the 90 level which defines the lower limit of a balanced market, 87.1 is the lowest level

since October 25, 2010. This means the market is the most favorable to buyers (and unfavorable to

sellers) in 14 years.

is not far below the 90 level which defines the lower limit of a balanced market, 87.1 is the lowest level

since October 25, 2010. This means the market is the most favorable to buyers (and unfavorable to

sellers) in 14 years.

We are still waiting for supply to stop growing. In most years this occurs no later than Thanksgiving.

Mid-Month Pricing Update and Forecast

Each month about this time we look back at the previous month, analyze how pricing has behaved and

report on how well our forecasting techniques performed. We also give a forecast for how the pricing

will move over the next month.

report on how well our forecasting techniques performed. We also give a forecast for how the pricing

will move over the next month.

For the monthly period ending November 15, we are currently recording sales of $/SF of $289.79

averaged for all areas and types across the ARMLS database. This is up 1.6% from the $285.20 we

now measure for October 15. Our forecast range mid-point was $286.78. We correctly forecast a rise,

but the size was somewhat larger than we anticipated - 1.6% rather than the 0.6% we calculated. The

actual result was well within the 90% confidence interval. The last 6 months have been extremely volatile

for price per sq. ft. - up nearly 5% one month and down 3% next. This is partly because of the lower

closing numbers. A smaller sample size tends to create more volatility in the averages. The median

sales prices have been much more stable since the high-end of the market has little to no effect on

medians.

averaged for all areas and types across the ARMLS database. This is up 1.6% from the $285.20 we

now measure for October 15. Our forecast range mid-point was $286.78. We correctly forecast a rise,

but the size was somewhat larger than we anticipated - 1.6% rather than the 0.6% we calculated. The

actual result was well within the 90% confidence interval. The last 6 months have been extremely volatile

for price per sq. ft. - up nearly 5% one month and down 3% next. This is partly because of the lower

closing numbers. A smaller sample size tends to create more volatility in the averages. The median

sales prices have been much more stable since the high-end of the market has little to no effect on

medians.

This latest increase is more in line with seasonal trends as we usually see an increase between October

and September.

and September.

On November 15 the pending listings for all areas & types show an average list $/SF of $333.17, up

1.5% from the reading for October 15. This suggests that closed prices will strengthen a little between

now and December. Among those pending listings we have 98.8% normal, 0.3% in REOs and 0.9% in

pre-foreclosures (including a very small number of short sales). The level of foreclosure activity has

picked up a little although it remains very low by long-term standards. Distress has certainly risen since

last month.

1.5% from the reading for October 15. This suggests that closed prices will strengthen a little between

now and December. Among those pending listings we have 98.8% normal, 0.3% in REOs and 0.9% in

pre-foreclosures (including a very small number of short sales). The level of foreclosure activity has

picked up a little although it remains very low by long-term standards. Distress has certainly risen since

last month.

Our mid-point forecast for the average monthly sales of $/SF on December 15 is $294.64, which is up

1.7% from the November 15 reading. We have 90% confidence that it will fall within ± 2% of this

midpoint, i.e. in the range $288.72 to $300.50.

1.7% from the November 15 reading. We have 90% confidence that it will fall within ± 2% of this

midpoint, i.e. in the range $288.72 to $300.50.

Currently demand is weak and stable while supply continues to rise. However, we would expect supply

to peak over the next week and then decline a little throughout the rest of 2024.

to peak over the next week and then decline a little throughout the rest of 2024.