Market Statistics Report for November 8, 2024

Market Dashboard – Dashboard

This Dashboard provides a comprehensive summary of the current state of the overall residential resale market.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

Daily Market Snapshot

The table below provides a concise statistical summary of today's residential resale market in the Phoenix metropolitan

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

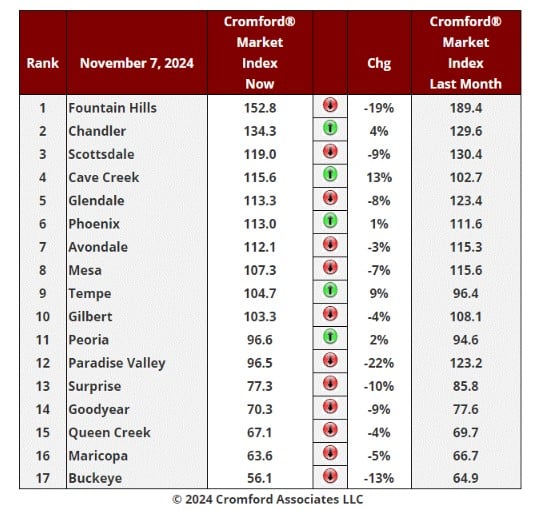

Cromford Market Index

Nov 7 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest

cities.

cities.

Cromford Market Index Commentary

There are still the same 5 large cities showing an increase in their Cromford® Market Index over the

past month. However, the average change in CMI over the past month is -5.0% while last week we saw

-4.8%. The market is deteriorating for sellers and slightly more quickly than last week.

past month. However, the average change in CMI over the past month is -5.0% while last week we saw

-4.8%. The market is deteriorating for sellers and slightly more quickly than last week.

Paradise Valley is once again the worst performer losing 22% over the most recent month but the good

news is that its CMI stabilized over the past week.

news is that its CMI stabilized over the past week.

Tempe and Cave Creek are sporting a respectable percentage gain of 9% or more, while the remaining

green dots are Chandler, Peoria and Phoenix. Fountain Hills is down 19%, though it is still comfortably

clear at the top of the table. Surprise and Buckeye remain among the weakest with downward moves

over 10%. Scottsdale has weakened significantly dropping 9%, as has Goodyear.

green dots are Chandler, Peoria and Phoenix. Fountain Hills is down 19%, though it is still comfortably

clear at the top of the table. Surprise and Buckeye remain among the weakest with downward moves

over 10%. Scottsdale has weakened significantly dropping 9%, as has Goodyear.

Currently we have 7 cities that are seller's markets, 5 that are balanced and 5 that are buyer's markets.

The trend remains negative. All 5 of the cities at the bottom of the table are down and sellers in these

areas are facing a considerable disadvantage in negotiations with buyers.

The trend remains negative. All 5 of the cities at the bottom of the table are down and sellers in these

areas are facing a considerable disadvantage in negotiations with buyers.

Among the secondary cities Anthem, Arizona City, Casa Grande, Laveen, Litchfield Park and Sun City

are buyer's market, while Gold Canyon, Sun City West and Sun Lakes are balanced. The sellers

markets are Apache Junction, El Mirage and Tolleson.

are buyer's market, while Gold Canyon, Sun City West and Sun Lakes are balanced. The sellers

markets are Apache Junction, El Mirage and Tolleson.

Multi Family Permits Commentary

Oct 26 - The third quarter of 2024 has been the quietest for multi-family permits since the second quarter

of 2023. At 3,142 multi-family units across Maricopa and Pinal counties, we are down 43% from the

third quarter of last year.

of 2023. At 3,142 multi-family units across Maricopa and Pinal counties, we are down 43% from the

third quarter of last year.

Year to date as of September 2024 we saw 11,315 units. This is down 22% from the same point last

year.

year.

It seems that multi-family investors have lost some of the enthusiasm they displayed between 2021 and

2023.

2023.

Foreclosure Commentary

Nov 6 - There were 416 residential foreclosure notices (Notices of Trustee Sale) in Maricopa County in

October. This is the highest monthly total since February 2020. For context this would have been

considered a low number prior to 2020, and October did have a high number of days for trustees to file

(23), but there is no denying we are seeing a rising trend in notices.

We also saw 55 foreclosure auctions (Trustee Sales), also the highest number since February 2020.

October. This is the highest monthly total since February 2020. For context this would have been

considered a low number prior to 2020, and October did have a high number of days for trustees to file

(23), but there is no denying we are seeing a rising trend in notices.

We also saw 55 foreclosure auctions (Trustee Sales), also the highest number since February 2020.

Prior to 2020, there were rarely fewer than 100 auctions a month, but we are seeing a rising trend here

too.

too.

Quite a few of the notices are for hard money loans taken out by fix and flip investors who are now

having trouble selling the property they borrowed against. Interest rates for hard money loans are very

high. They are called hard for a reason. So, borrowers can be quick to give up and allow the property

to go into foreclosure rather than come up with the high monthly repayments. These are not very

numerous, but it shows that fix and flip investment activity can sometimes be risky as well as sometimes

rewarding.

Affidavits of Value

having trouble selling the property they borrowed against. Interest rates for hard money loans are very

high. They are called hard for a reason. So, borrowers can be quick to give up and allow the property

to go into foreclosure rather than come up with the high monthly repayments. These are not very

numerous, but it shows that fix and flip investment activity can sometimes be risky as well as sometimes

rewarding.

Affidavits of Value

Nov 5 - The affidavits of value have been counted and analyzed for Maricopa County's October filings

and here is what we found:

and here is what we found:

• There were 6,150 closed transactions, up 11.0% from 5,543 in October 2023 and up 10.1% from

September.

• There were 1,502 closed new homes, up 1.4% from 1,481 in October 2023 and up 4.2% from

September.

• There were 4,648 closed re-sale transactions, up 14.4% from 4,062 in October 2023 and up 12.2% from

September.

• The overall median sales price in October was $475,000, up 2.5% from October 2023 and up 0.6% from

September.

• The new home median sales price was $525,506, up 3.3% from October 2023 and up 1.3% from

September.

• The re-sale median sales price was $455,000, up 2.4% from October 2023 and up 1.1% from

September.

September.

• There were 1,502 closed new homes, up 1.4% from 1,481 in October 2023 and up 4.2% from

September.

• There were 4,648 closed re-sale transactions, up 14.4% from 4,062 in October 2023 and up 12.2% from

September.

• The overall median sales price in October was $475,000, up 2.5% from October 2023 and up 0.6% from

September.

• The new home median sales price was $525,506, up 3.3% from October 2023 and up 1.3% from

September.

• The re-sale median sales price was $455,000, up 2.4% from October 2023 and up 1.1% from

September.

There were 23 working days in October 2024 versus 22 in October 2023, so the 11.0% increase in

closings was partly because of this tailwind. Re-sales jumped much more than new homes, which

actually went down if you allow for the tailwind. Given the drop in new home sales we saw last month,

the new home market appears to be losing speed.

closings was partly because of this tailwind. Re-sales jumped much more than new homes, which

actually went down if you allow for the tailwind. Given the drop in new home sales we saw last month,

the new home market appears to be losing speed.

In contrast, re-sale closings rose strongly compared to last month as well as year over year. This is a

consequence of the spike in contract activity in September that accompanied the drop-in interest

rates. Unfortunately, those interest rates have moved higher again, so we do not expect the trend to

continue into next month. The absence of a similar spike in new home closings is probably because

the average new home sales cycle is much longer. The home usually has to be completed before the

transaction is recorded, unless it is a spec that has already been finished.

consequence of the spike in contract activity in September that accompanied the drop-in interest

rates. Unfortunately, those interest rates have moved higher again, so we do not expect the trend to

continue into next month. The absence of a similar spike in new home closings is probably because

the average new home sales cycle is much longer. The home usually has to be completed before the

transaction is recorded, unless it is a spec that has already been finished.

New home market share fell to 24.4% in October 2024, and this is down from 26.7% a year ago.

Median prices were higher than last month and also higher than a year ago. But the combined peak

remains at $490,000 so we remain 3% below that level, which was achieved as long ago as May

2022.

remains at $490,000 so we remain 3% below that level, which was achieved as long ago as May

2022.

These numbers are for single family and townhouse / condo homes.

Affidavits of Value – Continued

Affidavits of Value – Continued

Nov 4 - Looking deeper into the contract ratios for price ranges we see the following.

This data is for single-family detached homes.

First, we can see that the contract ratio tends to fall as we move higher in price. This is always the

case and is particularly true of the highest price points where there are always a lot of homes listed for

sale compared with the very few contracts signed each month. It makes sense to compare contract

ratio readings for a segment over time, but less can be learned for comparing two different segments.

case and is particularly true of the highest price points where there are always a lot of homes listed for

sale compared with the very few contracts signed each month. It makes sense to compare contract

ratio readings for a segment over time, but less can be learned for comparing two different segments.

The following price ranges have seen exceptionally high falls in their contract ratios:

• Under $350K

• Between $2M and $3M

• Over $7.5M and especially over $10M

• Under $350K

• Between $2M and $3M

• Over $7.5M and especially over $10M

We can conclude that these segments have cooled more than the overall market over the last 12

months

months

The following show an increase in their contract ratios compared with a year ago:

• $1.5M to $2M

• $5M to $7.5M

• $1.5M to $2M

• $5M to $7.5M

These 2 segments are actually hotter than a year ago, bucking the general trend.