Market Statistics Report for October 13, 2024

Market Dashboard – Dashboard

This Dashboard provides a comprehensive summary of the current state of the overall residential resale market.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

commercial units, and multiple dwelling units are also excluded.

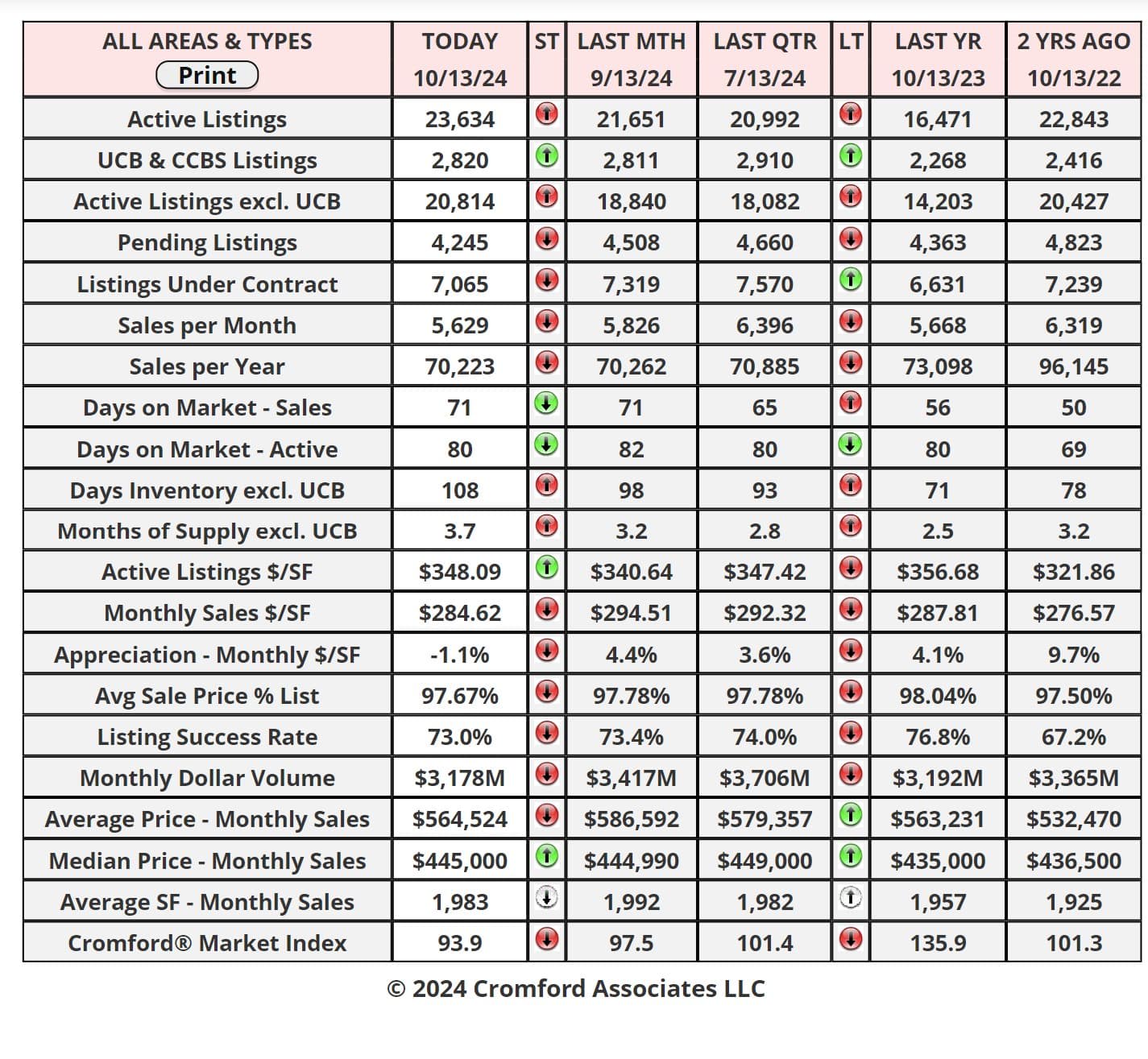

Daily Market Snapshot

The table below provides a concise statistical summary of today's residential resale market in the Phoenix metropolitan

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

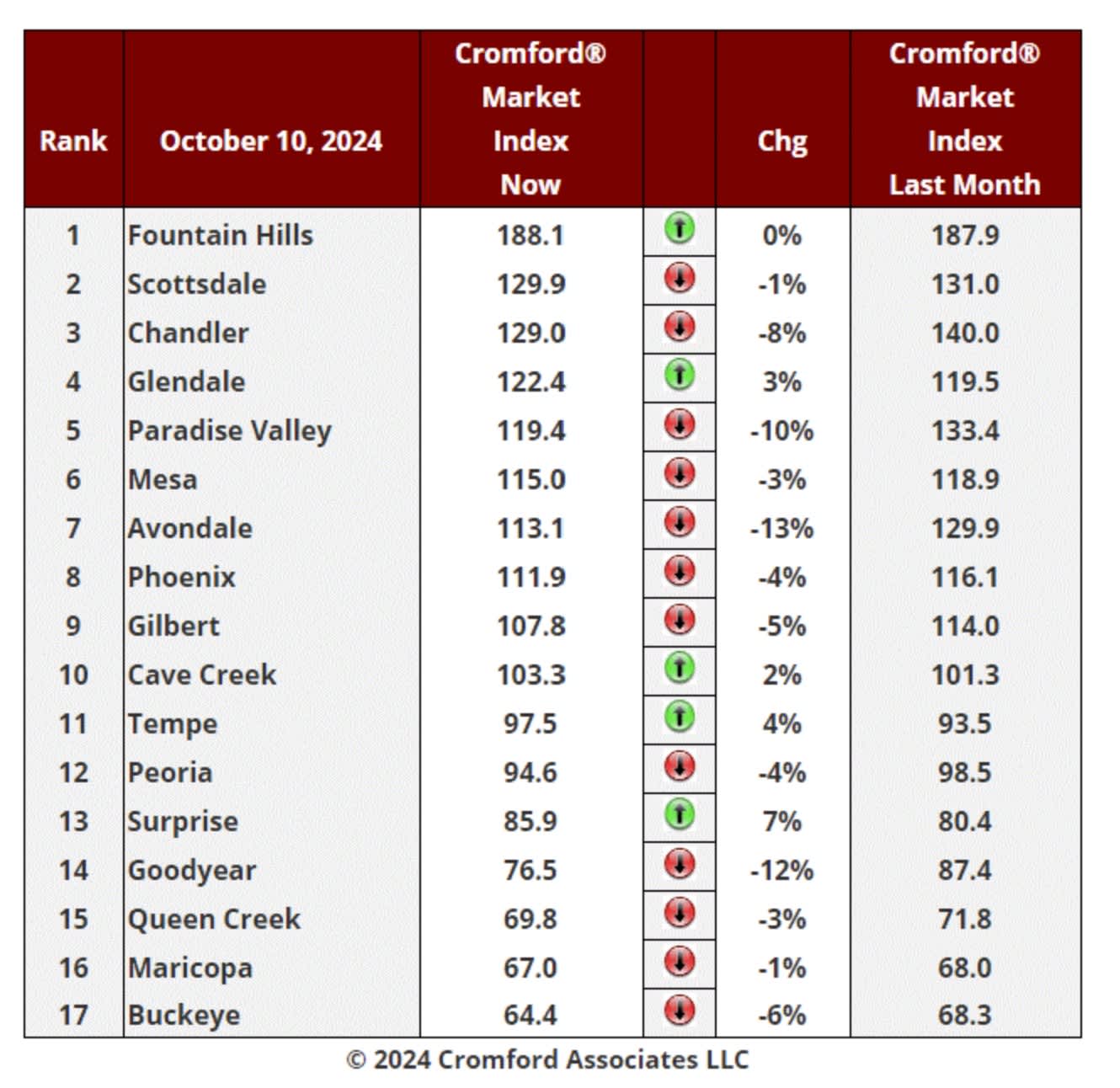

Cromford Market Index

Oct 10 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest

cities.

Cromford Market Index Commentary

Oct 10 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest

cities.

Cromford Market Index Commentary

Buyers are still gaining negotiation power as supply rises faster than demand.

There are now only 5 cities showing an increase in their Cromford® Market Index over the past month.

This is down from 6 a week ago. We have 12 cities showing a decrease and that includes the two largest

cities - Phoenix and Mesa.

This is down from 6 a week ago. We have 12 cities showing a decrease and that includes the two largest

cities - Phoenix and Mesa.

The average change in CMI over the past month is -3.3%. Last week we saw -2.7%. After a strong

period a month ago, Paradise Valley has quickly turned around and is one of the main decliners.

period a month ago, Paradise Valley has quickly turned around and is one of the main decliners.

Surprise is now the only city showing a respectable percentage gain of 7% or more, though it is still a

buyer's market. The remaining green dots are Fountain Hills, Glendale, Cave Creek and Tempe, but

they are up 3% or less. The largest declines are to be found in Avondale, Chandler, Paradise Valley

and Goodyear. A positive sign for sellers is that Phoenix is still just above the balanced zone below 110.

buyer's market. The remaining green dots are Fountain Hills, Glendale, Cave Creek and Tempe, but

they are up 3% or less. The largest declines are to be found in Avondale, Chandler, Paradise Valley

and Goodyear. A positive sign for sellers is that Phoenix is still just above the balanced zone below 110.

8 out of 17 cities remain seller's markets over 110, though 4 of these are below 120. We have 4 cities

that are balanced, while the remaining 5 are buyer's markets. Only 1 city is still over 140, but 3 are

below 70.

that are balanced, while the remaining 5 are buyer's markets. Only 1 city is still over 140, but 3 are

below 70.

Mortgage Rate Commentary

Oct 8 - The majority of people thought that mortgage rates would go down after the Federal Reserve

cut their base rate 3 weeks ago. The majority have been wrong so far. Last Friday's jobs report

suggested that the USA economy was stronger than expected and added more upward momentum to

mortgage interest rates.

cut their base rate 3 weeks ago. The majority have been wrong so far. Last Friday's jobs report

suggested that the USA economy was stronger than expected and added more upward momentum to

mortgage interest rates.

We now have the highest rates in 2 months with the 30-year fixed at around 6.62%.

Meanwhile active supply increased 3.7% over the past week, so buyer's have more homes to

choose from. The market trend in most areas is still favoring buyers over sellers.

choose from. The market trend in most areas is still favoring buyers over sellers.

Affidavits of Value

Oct 6 - The affidavits of value have been counted and analyzed for Maricopa County's September

filings and here is what we found:

• There were 5,584 closed transactions, down 5.3% from 5,896 in September 2023 and down 6.4% from

August.

• There were 1,441 closed new homes, down 11.3% from 1,624 in September 2023 and down 0.8% from

August.

• There were 4,143 closed re-sale transactions, down 3.0% from 4,272 in September 2023 and down

8.2% from August.

• The overall median sales price in September was $471,995, up 4.9% from September 2023 and up

0.4% from August.

• The re-sale median sales price was $450,000, up 2.3% from September 2023 but unchanged from

August.

• The new home median sales price was $518,792, up 8.3% from September 2023 and up 1.0% from

August.

There were 21 working days in September 2024 versus 20 in September 2023, so the 5.3% drop in

closings is actually worse than it looks. We would expect a 5.0% increase if the same closing rate per

day were applied.

filings and here is what we found:

• There were 5,584 closed transactions, down 5.3% from 5,896 in September 2023 and down 6.4% from

August.

• There were 1,441 closed new homes, down 11.3% from 1,624 in September 2023 and down 0.8% from

August.

• There were 4,143 closed re-sale transactions, down 3.0% from 4,272 in September 2023 and down

8.2% from August.

• The overall median sales price in September was $471,995, up 4.9% from September 2023 and up

0.4% from August.

• The re-sale median sales price was $450,000, up 2.3% from September 2023 but unchanged from

August.

• The new home median sales price was $518,792, up 8.3% from September 2023 and up 1.0% from

August.

There were 21 working days in September 2024 versus 20 in September 2023, so the 5.3% drop in

closings is actually worse than it looks. We would expect a 5.0% increase if the same closing rate per

day were applied.

New home closings fell harder year over year with a drop of 11.3%, while resales fell only 0.8%.

However, closing volumes were poor across the board in September.

However, closing volumes were poor across the board in September.

New home market share rose to a strong 25.8% in September 2024, but this is down from 27.5% a

year ago.

year ago.

Prices bounced back a little compared with August. The combined peak remains at $490,000 so we

remain 3.7% below that level achieved in May 2022.

remain 3.7% below that level achieved in May 2022.

The general picture is of low volumes but stable pricing. The outlook is for volume to improve a bit and

for prices to remain stable with a slight downward tendency due to the slight excess of supply over

demand.

for prices to remain stable with a slight downward tendency due to the slight excess of supply over

demand.

These numbers are for single family and townhouse / condo homes.