Market Statistics Report for October 30, 2024

Market Dashboard – Dashboard

This Dashboard provides a comprehensive summary of the current state of the overall residential resale market.

All the statistics shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

recorded by ARMLS are included. Geographically, this includes Maricopa County, a large part of Pinal County and a small

part of Yavapai county. In addition, "out of area" listings recorded on ARMLS are included, although these usually

constitute a very small percentage of total sales and have very little effect on the data.

All dwelling types are included. For-sale-by-owner, auctions and other non-MLS transactions are not included. Land,

commercial units, and multiple dwelling units are also excluded.

commercial units, and multiple dwelling units are also excluded.

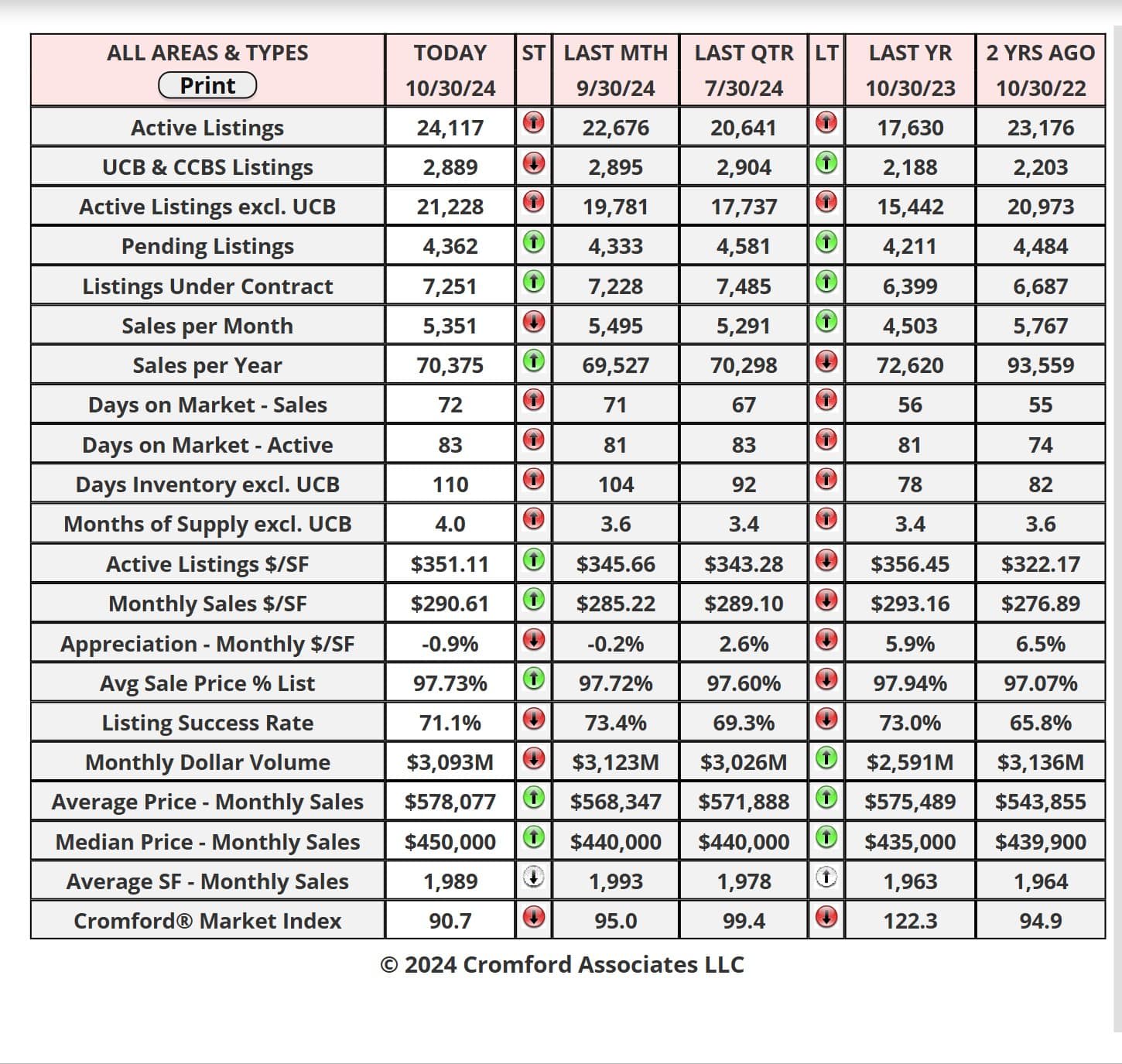

Daily Market Snapshot

The table below provides a concise statistical summary of today's residential resale market in the Phoenix metropolitan

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

area. The figures shown are for the entire Arizona Regional area as defined by ARMLS. All residential resale transactions

recorded by ARMLS are included. Geographically, this includes Maricopa county, the majority of Pinal county and a small

part of Yavapai county. In addition, "out of area" listings recorded in ARMLS are included, although these constitute a very

small percentage (typically less than 1%) of total sales and have very little effect on the statistics.

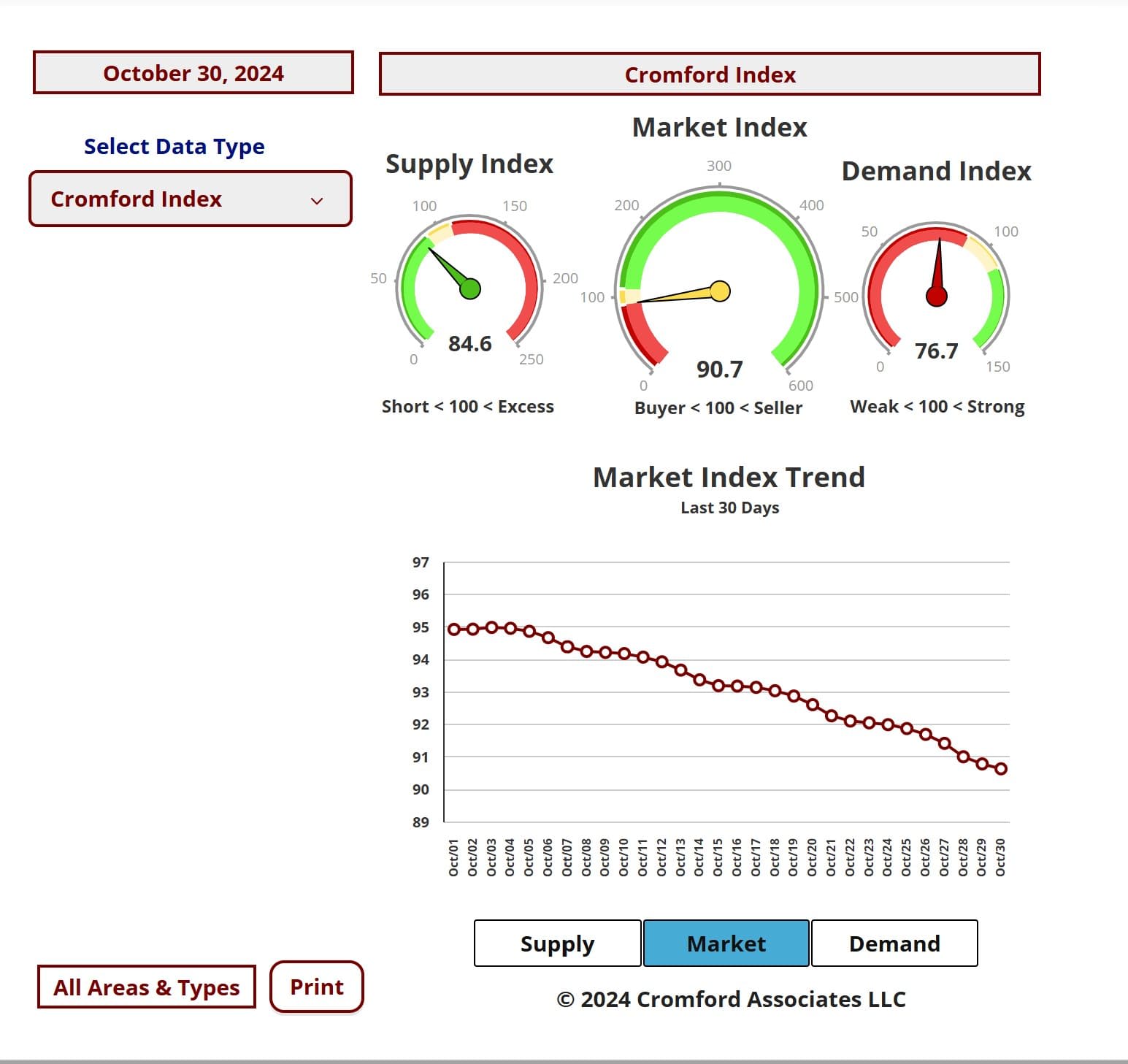

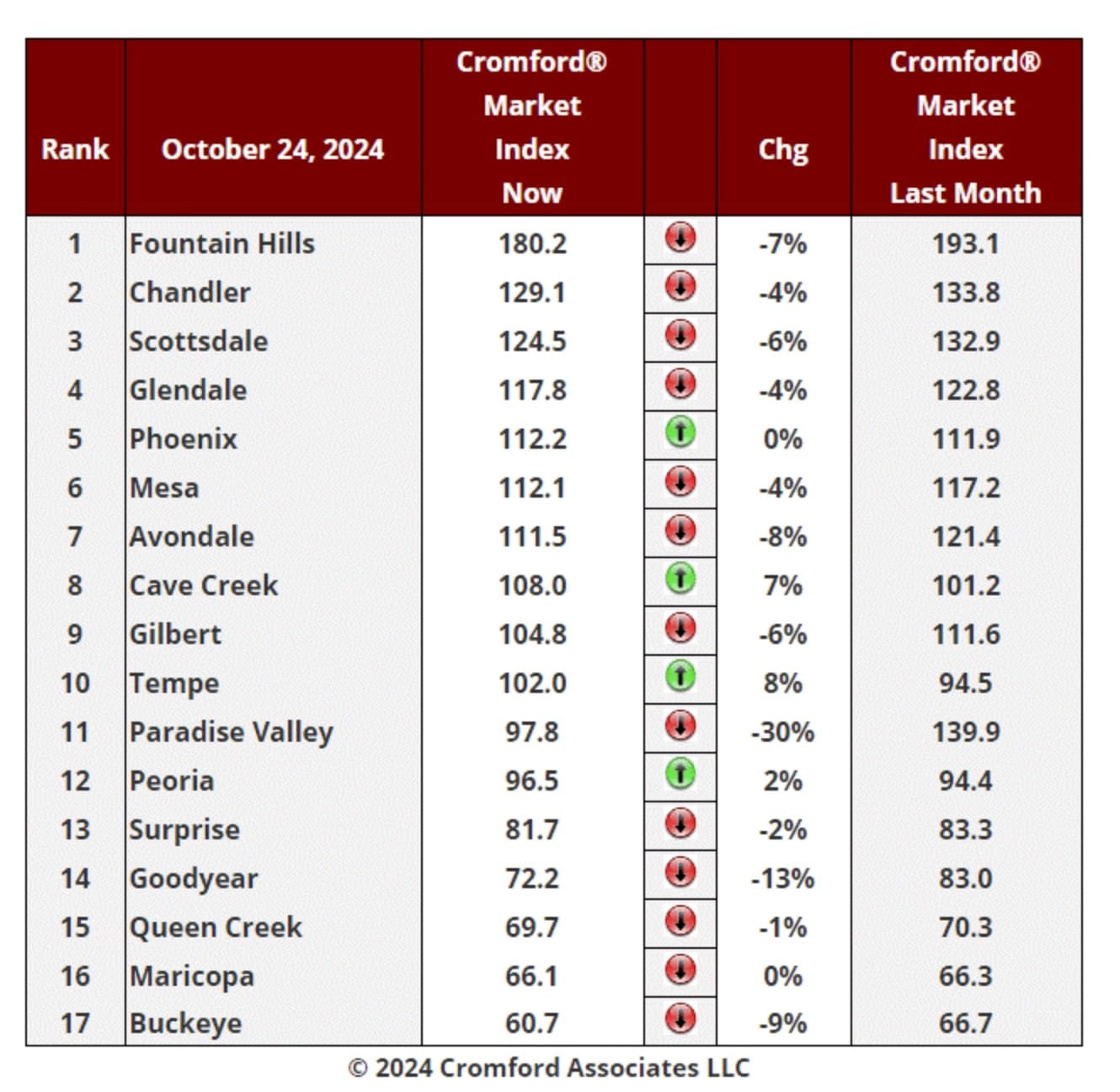

Cromford Market Index

Oct 24 - Here is our latest table of Cromford® Market Index values for the single-family markets in the 17 largest

cities.

Cromford Market Index Commentary

The mortgage rate news has been bad over the last week with the typical 30-year fixed rate around

6.91% today, having been 6.68% last week. It is all the way back up to the level we saw in late July.

6.91% today, having been 6.68% last week. It is all the way back up to the level we saw in late July.

There are once again only 4 large cities showing an increase in their Cromford® Market Index over the

past month. However, it is not quite the same 4 as last week. Maricopa has dropped out and been

replaced by Phoenix. We have 13 cities showing a decrease and the fact that Phoenix is not among

them is a good thing, as it accounts for roughly 25% of all transactions in our area.

past month. However, it is not quite the same 4 as last week. Maricopa has dropped out and been

replaced by Phoenix. We have 13 cities showing a decrease and the fact that Phoenix is not among

them is a good thing, as it accounts for roughly 25% of all transactions in our area.

On the other hand, the average change in CMI over the past month is -4.5% while last week we saw -

4.0%. Paradise Valley is by far the worst performer, losing 30% over the most recent month.

4.0%. Paradise Valley is by far the worst performer, losing 30% over the most recent month.

Tempe has been joined by Cave Creek in showing a respectable percentage gain of 7% or more, while

the remaining green dots are Peoria and Phoenix. Excluding PV, the largest declines are again found

in the Southwest - Avondale, Goodyear and Buckeye.

the remaining green dots are Peoria and Phoenix. Excluding PV, the largest declines are again found

in the Southwest - Avondale, Goodyear and Buckeye.

Multi Family Permits Commentary

Oct 26 - The third quarter of 2024 has been the quietest for multi-family permits since the second quarter

of 2023. At 3,142 multi-family units across Maricopa and Pinal counties, we are down 43% from the

third quarter of last year.

of 2023. At 3,142 multi-family units across Maricopa and Pinal counties, we are down 43% from the

third quarter of last year.

Year to date as of September 2024 we saw 11,315 units. This is down 22% from the same point last

year.

year.

It seems that multi-family investors have lost some of the enthusiasm they displayed between 2021 and

2023.

2023.

S&P / Case-Shiller Home Price Index

Oct 29 - The latest S&P / Case-Shiller® Home Price Index® numbers were published this Tuesday.

The new report covers home sales during the period June to August 2024. This means the typical home

sale closed in mid-July, more than 3 months ago. Please remember that Case-Shiller data is fairly old,

even on the day it is released.

The new report covers home sales during the period June to August 2024. This means the typical home

sale closed in mid-July, more than 3 months ago. Please remember that Case-Shiller data is fairly old,

even on the day it is released.

Two months ago, all 20 cities showed rising prices but this month 17 of them went down over the month.

Compared with the previous month's series we see the following changes:

1. Chicago +0.43%

2. Las Vegas +0.21%

3. Detroit +0.15%

4. Charlotte -0.02%

5. Atlanta -0.03%

6. Phoenix -0.10%

7. Miami -0.10%

8. New York -0.12%

9. Washington -0.15%

10. Portland -0.16%

11. Minneapolis -0.17%

12. Tampa -0.21%

13. Cleveland -0.24%

14. Boston -0.29%

15. Seattle -0.45%

16. Dallas -0.47%

17. Los Angeles -0.66%

18. San Diego -0.67%

19. Denver -0.71%

20. San Francisco -1.15%

1. Chicago +0.43%

2. Las Vegas +0.21%

3. Detroit +0.15%

4. Charlotte -0.02%

5. Atlanta -0.03%

6. Phoenix -0.10%

7. Miami -0.10%

8. New York -0.12%

9. Washington -0.15%

10. Portland -0.16%

11. Minneapolis -0.17%

12. Tampa -0.21%

13. Cleveland -0.24%

14. Boston -0.29%

15. Seattle -0.45%

16. Dallas -0.47%

17. Los Angeles -0.66%

18. San Diego -0.67%

19. Denver -0.71%

20. San Francisco -1.15%

Phoenix has risen from 11th to 6th place over the last month. The national average was -0.13% so Phoenix was slightly better than this average.

The only cities still rising were Chicago, Las Vegas and Detroit.

Comparing year over year, we see the following changes:

1. New York +8.1%

2. Las Vegas +7.3%

3. Chicago +7.2%

4. Cleveland +6.9%

5. Detroit +6.0%

6. Los Angeles +5.9%

7. San Diego +5.7%

8. Boston +5.5%

9. Washington +5.4%

10. Seattle +5.2%

11. Miami +5.1%

12. Charlotte +5.0%

13. Atlanta +3.7%

14. San Francisco +2.8%

15. Phoenix +2.1%

16. Minneapolis +2.%

17. Tampa +1.7%

18. Dallas +1.6%

19. Portland +0.8%

20. Denver +0.7%

1. New York +8.1%

2. Las Vegas +7.3%

3. Chicago +7.2%

4. Cleveland +6.9%

5. Detroit +6.0%

6. Los Angeles +5.9%

7. San Diego +5.7%

8. Boston +5.5%

9. Washington +5.4%

10. Seattle +5.2%

11. Miami +5.1%

12. Charlotte +5.0%

13. Atlanta +3.7%

14. San Francisco +2.8%

15. Phoenix +2.1%

16. Minneapolis +2.%

17. Tampa +1.7%

18. Dallas +1.6%

19. Portland +0.8%

20. Denver +0.7%

Phoenix stayed at 15th place once again and is still stuck in the bottom half on a year over year basis.

All 20 of the cities are again showing positive price movement from one year ago with Denver and Portland again at the bottom. Las Vegas looks very strong in both tables.

The national average is +4.2% year over year. Phoenix is at half that percentage, so has

underperformed over the last 12 years.

underperformed over the last 12 years.